- P-ISSN 2586-2995

- E-ISSN 2586-4130

This study analyzes global inflation synchronization and derives policy implications for the Korean economy. Unlike previous studies that assume a single global inflation factor, this study investigates if inflation in Korea can be explained further by other global inflation factors. Our principal component analysis provides three principal components for global inflation that are linked to the Korea inflation rate ― the first component is closely related to OECD inflation, and the second and third components reflect China’s inflation. This study empirically demonstrates via in-sample fitting and out-of-sample forecasting that the three principal components of global inflation play a significant role in explaining and predicting Korean inflation in the short-term, while their role is limited in the mid-term. Domestic macroeconomic variables are found to be more important for the mid-term movements of the Korean inflation rate. The empirical results here suggest that the Bank of Korea should focus more on domestic economic conditions than on global inflation when implementing monetary policy because global factors are likely to be already reflected in domestic macro-variables in the mid-term.

Inflation Rates, Monetary Policy, Forecasting, Principal Component Model, LASSO

E31, E37, E5

Many theoretical inflation models, represented by the Phillips curve, predict that there exists a meaningful relationship between economy activity and inflation. However, recent studies provide empirical evidence that the link between the real economy and inflation has weakened or disappeared since early 2000s. The macroeconomic phenomenon which casts doubt on the theoretical prediction is referred to as the ‘missing disinflation puzzle’. Regarding new empirical findings, special attention is paid to the role of a global inflation factor that triggers simultaneous movements in many countries’ inflation rates. Many studies in the literature argue that the missing disinflation puzzle is partially attributed to the changed importance of the global inflation factor in recent decades (e.g., Ciccarelli and Mojon, 2010; Mumtaz and Surico, 2012; Mikolajun and Lodge, 2016).

Global inflation synchronization is also linked to the low inflation rates commonly observed in major developed countries approximately since 2012. For instance, inflation rates were close to 0% in European countries and in the United States during this period. Sluggish inflation raises concern about deflation along with prolonged economic downturns, motivating central banks to implement non-traditional monetary policies such as massive quantitative easing to bring inflation rates up to their target rates. This new policy instrument has led to a sharp rise in asset prices in the capital markets via the excessive liquidity supply and low interest rates. As such, global inflation synchronization has a deep connection not only to inflation but also to various parts of the economy. Currently, many studies, such as that by Constâncio (2014), are underway. Moreover, central banks and international organizations are closely watching this unprecedented phenomenon. Related to this Hall (2011) and Christiano et al. (2015) study how low inflation and a slow economic recovery are connected to the causes of the Great Recession.

The aim of this study is to suggest policy implications for the Korean economy associated with global inflation synchronization. Considering that the Korean economy heavily relies on international trade, it would be important to understand how the global phenomenon affects inflation in Korea. The Korea inflation rate has continued to fall below the Bank of Korea's inflation target rate in recent years. This could be a natural consequence of Korea being more affected by the low level of the global inflation factor rather than by certain domestic factors.

This study is related to previous studies in the literature. Ciccarelli and Mojon (2010) empirically demonstrate that a single global inflation factor can suitably explain the inflation rates of many countries and allows for improved inflation forecasting. Borio and Filardo (2007) show that structural changes in the global aggregate demand explain global inflation dynamics. Melitz and Ottaviano (2008) point to trade liberalization as a source of global inflation synchronization. Cecchetti et al. (2007), Rogoff (2003), Mumtaz and Surico (2012), and Conti et al. (2017) emphasize the role of traditional monetary policies on inflation synchronization and low inflation. Mumtaz and Surico (2012) show that the low inflation has been commonly observed in many developed countries since 1980s and argue that such a change in the inflation dynamics is directly linked to global currency depreciation. Lastly, Mikolajun and Lodge (2016) provide evidence that a global inflation factor explains the inflation rates of individual countries well, but the influence of the global factor is already absorbed in domestic macro-variables. They conclude that there is no need to consider the global factor separately when explaining the inflation rates of individual countries.

Unlike the aforementioned papers, this study considers the possibility that there exist several global inflation factors rather than just one. To extract potential factors, a principal component analysis (PCA) is applied to panel data of inflation rates and the estimated principal components are then employed to explain and predict Korean inflation rates. A particularly striking result is that the first principal component is closely related to the OECD weighted average inflation rate, while the second and third principal components are closely related to China’s inflation rate.

One of the difficulties in an empirical analysis of Korean inflation is that the sample size of Korean macroeconomic variables is not yet sufficiently accumulated for reliable statistical inference, as the Bank of Korea changed its monetary policy base to inflation targeting in 1998. Due to the lack of data information, it is practically difficult to carry out a precise quantitative analysis in empirical models in which both global inflation factors and domestic macro-variables are included. This study resolves this practical issue by employing the LASSO (Least Absolute Shrinkage and Selection Operator) methodology of Tibshirani (1996). LASSO is a widely used technique in the machine learning literature in cases involving a limited amount of data compared to the number of coefficients.

The main empirical findings of this study are as follows. The global inflation principal components play important roles in explaining and predicting Korea's inflation rate in the short-term. However, in the mid-term, the performance of the global inflation principal components in terms of in-sample fitting and out-of-sample forecasting substantially diminishes. On the other hand, Korean macro-variables provide better explanatory and prediction power in the mid-term than the global inflation principal components. In light of this point, the recent economic downturn in the global economy and the resulting low global inflation may have only a limited effect on the inflation rate in Korea in the mid-term. In addition, the Bank of Korea, whose policy goal is to keep domestic prices stable, appears to be more apt to adjust its monetary policy in accordance with Korean economic situations. However, this does not necessarily mean that the Bank of Korea should ignore global inflation factors. Rather, it means that because global factors change Korean macro-variables in the mid-term, it is better carefully to monitor the macro-variables which already reflect global economic conditions when enacting its monetary policies.

The composition of this paper is as follows. In Section 2, we examine the inflation synchronization phenomenon using panel data for inflation rates. Also, we estimate the global inflation factors via PCA and shows how inflation in each individual country is explained by common factors. In Section 3, international and domestic macro-variables relevant to the inflation rate of Korea are extracted from LASSO. Section 4 discusses policy implications based on the results of Sections 2 and 3. Section 5 provides concluding remarks.

Researchers have been actively investigating global synchronization in the real economy and inflation since the early 2000s. A representative study is that by Ciccarelli and Mojon (2010). They argue that similar patterns in long-term inflation trends are observed in many developed countries.

Figure 1 and Figure 2 show the inflation trends of major developed countries (G7) and Korea. As shown in the figure, inflation in developed countries has shown a highly consistent trend since the late 1990s. Clearer co-movements are observed during the financial crisis. The Korean inflation rate has also been characterized by inflation synchronization since the late 1990s. One noticeable feature is that inflation synchronization exists not only in the mid-term (annual inflation rate in Figure 2) but also in the very short-term (quarterly inflation rate in Figure 1).

Note: The solid black line indicates the inflation rate of Korea.

Source: OECD (https://data.oecd.org/price/inflation-cpi.htm, accessed: 15 October 2018). Sample period: Q1 1985 to Q2 2018.

Note: The solid black line indicates the inflation rate of Korea.

Source: OECD (https://data.oecd.org/price/inflation-cpi.htm, accessed: 15 October 2018). Sample period: Q4 1985 to Q2 2018.

To demonstrate empirically the rise of inflation synchronization further, the inflation rates of 22 OECD countries and China are reported in Figure 3. The 22 OECD countries are Austria, Australia, Belgium, Canada, Denmark, Finland, France, Germany, Greece, Italy, Ireland, Japan, Luxembourg, Netherland, New Zealand, Norway, Portugal, Spain, Sweden, Switzerland, U.K., and the United States. The OECD countries were also used in the study of Ciccarelli and Mojon (2010).

It is clear that inflation in OECD countries has seen constantly showing very similar movements since the late 1990s, as in the case of the G7 countries. Next, in Figure 4 we report how the cross-sectional variance of the inflation rates changes over time. At each quarter, the sample variance is calculated using the inflation rates in Figure 3. The inflation variance continues to fall since the mid-1980s, reaching 0.5 and less since the late 1990s. This can be interpreted as meaning that the inflation rates have varied similarly relative to each other for the last 20 years.

Note: 1) The solid black line indicates the inflation rate of Korea, 2) The dotted lines indicate the inflation rates of other OECD countries, 3) Only OECD countries included in the study by Ciccarelli and Mojon (2010) are included in the data.

Source: OECD (https://data.oecd.org/price/inflation-cpi.htm, accessed: 15 October 2018). Sample period: Q1 1985 to Q2 2018.

Source: OECD (https://data.oecd.org/price/inflation-cpi.htm, accessed: 15 October 2018). Sample period: Q1 1985 to Q2 2018.

In order to check how the correlation between Korean inflation and other OECD countries’ inflation rates has been changing over time properly, which is the main goal of this study, the full sample period is divided into sections before and after 1998. Note that the Bank of Korea began inflation targeting in 1998. The sample correlation is computed using pairs of the inflation rates between Korea and each OECD country. The average of the sample correlations is used for the analysis. Before 1998, China's inflation rate is excluded in the computation. The average correlation before 1998 is only 0.098, while it is 0.27 after 1998. This means that the correlation between Korean inflation and inflation in other OECD countries has increased dramatically over the last 20 years.

Currently, the central banks of major developed countries are implementing inflation targeting, that is, monetary policy intended to hold inflation to a moderate level. However, these central bank policies have not been successful. Table 1 shows the annual inflation target levels of selected major countries and Korea from 2012 to 2016. Also see Figure 5 for how much actual inflation rates deviate from the target rates in the developed countries. It is clearly shown in Figure 5 that the actual inflation rate in Korea substantially differs from the target rate set by the Bank of Korea from 2012 to 2016. Despite the fact that the deviation of actual inflation from its target rate is persistent, its underlying cause has not yet been identified. However, the global inflation synchronization shown in Figures 1-4 suggests the possibility that some global factors not controlled by the monetary policy of the Bank of Korea may influence the inflation rate in Korea.

Note: When the inflation stability target is reported as a range, i.e., other than a single point, the median value of the range is reported here.

Source: 1) The inflation stability targets for the major developed countries are described in Contessi et al. (2014). 2) The Bank of Korea (https://ecos.bok.or.kr/, accessed: 15 October 2018). 3) OECD (https://data.oecd.org/price/infla tion-cpi.htm, accessed: October 15, 2018).

Note: When the inflation stability target is reported as a range, i.e., other than a single point, the median value of the range is reported here. The numbers in the left column are years for the data.

Source: 1) The inflation stability targets for the major developed countries are described in Contessi et al. (2014). 2) The Bank of Korea (https://ecos.bok.or.kr/, accessed: 15 October 2018). 3) OECD (https://data.oecd.org/price/infla tion-cpi.htm, accessed: October 15, 2018).

This section focuses on the effect of global inflation synchronization on CPI (consumer price index) inflation in Korea. To extract a global inflation factor, Ciccarelli and Mojon (2010) conducted a dynamic factor analysis to the 22 OECD countries mentioned in the previous section. Their study provides evidence that a single global inflation factor accounts for 50% to 90% of inflation movements in many countries. The result is especially noticeable for developed countries.

Ciccarelli and Mojon (2010) assume that only one global inflation factor matters in the explanation of the inflation rates of individual countries. In order to validate this assumption empirically, this study carefully examines five independent principal components as potential global factors that can explain Korean inflation. It is important to note that the main goal of this analysis is not statistically to choose the correct number of common factors. A principal component that does not have strong in-sample explanatory power for other countries may have strong in-sample explanatory or out-of-sample forecasting power with regard to Korean inflation.

This study estimates several global inflation factors through a principal component analysis (PCA). The factor analysis used in Ciccarelli and Mojon (2010) is relatively easy to interpret in that it assumes that while a global factor affects all individual countries, idiosyncratic shocks to individual countries cannot affect the global factor. However, as the number of common factors increases in the factor model, the number of coefficients to be estimated rapidly increases. It is also necessary to make strong assumptions about how each common factor evolves over time and about how common factors differ from each other. China’s inflation data used in our analysis are available only from the mid-1990s in the World Bank database. Therefore, inaccurate estimates are likely due to the lack of data if we adopt the dynamic factor model of Ciccarelli and Mojon (2010). On the other hand, PCA, which is a non-parametric estimation method, does not require us to estimate many coefficients for statistical inference compared to the number of observations. Many papers, such as that by Stock and Watson (2011), theoretically show that the principal components of PCA well approximate common factors of a factor analysis when the cross-section sample size is large enough. Although the cross-section sample size of the data of this study is not that large, we obtain empirical evidence by which the first principal component resembles the OECD average inflation rate, consistent with other studies showing that the common factor estimated by dynamic factor models is nearly identical to the OECD average inflation rate.

The j -th principal component is given by a linear function of the inflation rates (y1,t, y2,t, ⋯, yn,t) of n countries, and each principal component is constructed by different weights (wj,1, wj,2, ⋯, yj,n, j = 1, 2, ⋯, 5), as follows:

The first principal component ( f1,t ) is the component that best describes the inflation rates of n countries collectively. The order of the other principal components is determined according to their in-sample explanatory power levels.

In addition to the inflation data from the 22 OECD countries used in Ciccarelli and Mojon (2010), our study estimates the principal components with China’s CPI inflation rate. China's share of exports in international trade has increased significantly over the past two decades. This simply means that the Chinese economy now has a non-negligible influence in the global market. Therefore, excluding China in the analysis, as in Ciccarelli and Mojon (2010), could result in misleading policy implications. Therefore, this study additionally considers the linkage of the global economy with China.

Table 2 shows how well the five principal components account for the inflation rates for all countries in the sample and for certain selected developed countries. The first component accounts for approximately 50% of the inflation rate panel data. The second and third components account for 7.6% and 5.2% of the data, respectively. On average, the first three components explain about 63% of the world's inflation rates.

From the third column to the last column, Table 2 shows the in-sample explanatory power levels of the five components for the major developed countries. Ciccarelli and Mojon (2010) argue that a single global inflation factor (or the first principal component) has more explanatory power compared to the result in Table 2. There are two reasons for this difference. Firstly, Ciccarelli and Mojon (2010) intensively analyze the inflation dynamics before the 2008 financial crisis, while this study adds more data collected over the past ten years. Secondly, unlike the common factor analysis of Ciccarelli and Mojon (2010), PCA assumes several independent components; consequently, each component could have less explanatory power than a single common factor extracted by their common factor analysis.

Note: 1) The weights that construct the principal components are estimated using data from the first quarter of 1998 to the second quarter of 2018. 2) In order to avoid the quantitative problem of the domestic price prediction model to be used in Section 2, such as the redundant use of data, the domestic consumer price is not used to estimate the principal component.

Source: CPI inflation rate data - World Bank (https://data.worldbank.org/, accessed: October 15, 2018), Estimates – author's calculations.

A drawback of PCA is that interpretations of the estimated principal components are difficult. To resolve the interpretation issue, we examine how countries' first, second and third principal components are largely reflected. Figure 6 reports the absolute values of the estimated weights of the principal components.

Figure 6 shows that the first principal component widely reflects inflation in the major developed countries. The second and third principal components reflect China’s inflation. This implies that an empirical analysis without China’s inflation data could lead to statistical errors. This result may be viewed as a natural consequence of the Chinese economy having significant impacts on the global economy since the 1990s.

Note: fi represents the ith component.

Source: Inflation data - World Bank, weights for principal components - author's calculations.

Figure 7 shows the weighted average of OECD countries’ inflation rates according to the real GDP and the estimated first principal component. Except one or two years in the late 1990s, the two series show nearly identical movements. Ciccarelli and Mojon (2010) also empirically demonstrate that the single global inflation factor is nearly identical to the OECD inflation rate. Figure 7 implies that the first principal component estimated in this study also can be interpreted as the global inflation factor estimated by Ciccarelli and Mojon (2010).

Note: pca1: first principal component; OECD: OECD Inflation.

Source: author's calculations.

Figure 8 shows that the second and third principal components collectively contain information about China’s inflation. In Figure 8, the blue line represents the difference between the second and third principal components, and the red line represents China’s inflation rate. The result that the linear combination of the two principal components represents inflation in China and these components explain inflation at a rate of approximately 13% of the major OECD countries has not been published in previous studies.

Note: pca2: second principal component; pca3: third principal component; china: China’s inflation rate.

Source: author's calculations.

Lastly, in PCA, a mathematical sign is not meaningless. Consequently, it is possible to multiply the second principal component by -1 and define it as a new principal component. Accordingly, China’s inflation rate can be seen as the sum of the third and newly defined second principal component.

The fourth and fifth principal components may also have important meanings, but a direct interpretation is not necessary because they are not selected by our statistical procedure in the models that explain Korea’s inflation rate in the next section.

The parallel analysis developed by Horn (1965) has been widely used to determine the number of principal components or common factors in practice. See O’Connor (2000), Dinno (2009), and Dobriban and Owen (2019) for details about this implementation and recent developments. The method is based on the eigenvalues of the covariance matrix for bootstrapped samples. In the test, each eigenvalue extracted from the actual data is compared to a set of counterpart eigenvalues extracted from randomly generated data sets via bootstrapping. If the actual eigenvalue is larger than a percentile of the simulated eigenvalues pre-specified by a researcher, the principal component corresponding to the tested eigenvalue is statistically significant. With a cutoff percentile of 0.95, the parallel analysis indicates that only the first principal component is statistically significant, whereas the second and third principal components are not. The critical values are estimated to be 2.178, 1.952, and 1.796 for the first three principal components. The actual eigenvalues are estimated to be 10.906, 1.788 and 1.188 for the first three principal components. This result is not surprising given that the second and third principal components explain only 7.6% and 5.2% of the whole dataset, as shown in Table 2. However, the main objective of this study is not to determine the number of statistically significant principal components. Instead, the main goal is to determine the presence of one or more common factors that can explain the Korea inflation rate. Despite the fact that the parallel analysis suggests only a single common factor, it does not necessarily mean that other factors are meaningless with regard to the Korean inflation rate.

Korea’s inflation and the three estimated principal components are compared directly in Figure 9. To simplify this comparison, Korea’s inflation rate and the estimated principal components are normalized. The first principal component shows movements similar to those of Korea’s inflation rate in the short-term and long-term. However, it is difficult to find direct relationships between the second or third principal component and Korea’s inflation rate through a visual inspection. In the next section, a detailed statistical analysis of the relationship between Korea’s inflation rate and the principal components will be conducted. Another interesting finding in this section is that the correlation between Korea’s inflation rate and the first principal component changes before and after 1998. The sample correlation is - 0.17 before 1998 and increases to 0.63 after 1998.

Note: Korea CPI price - Bank of Korea.

Source: author's calculations.

For a robustness check, PCA is conducted using expanded inflation rate data from the Czech Republic, Mexico, Poland, and Korea in addition to the 22 OECD countries used in Ciccarelli and Mojon (2010). This result is reported in Table 3 and Figure 10. As before, the first principal component accounts for 45% of the inflation rate movements in all of the countries included in the analysis.

A notable difference can be found in the interpretation of the second and third principal components. As shown in Figure 10, the second principal component is mainly formed by China’s inflation rate, as before. However, the third principal component is driven in large part by Japan’s inflation rate. The third principal component reported in Figure 10 is most likely related to the fourth or fifth principal component obtained from the previous PCA. This can be deduced from the result in Table 3, which shows that the fourth and fifth principal components well explain Japan's inflation rate.

Note: 1) The weights used to construct the principal components are estimated using data from the first quarter of 1998 to the second quarter of 2018.

Source: CPI - World Bank; Estimates - author’s calculations.

Note: fi represents the ith component.

Source: Inflation data - World Bank, weights for principal components - author's calculations.

Next, we compare the first and second principal components estimated by the expanded data. Figure 11 clearly shows that the first principal component and the OECD inflation rate are nearly identical, as before. Moreover, in Figure 12, the second principal component and China's inflation rate move very similarly in the mid-term and long-term. This means that although there are subtle differences between the results of the original data and the expanded data, China’s inflation rate is directly related to the underlying principal components.

The goal of this section is to analyze the economic variables that explain global inflation. To this end, we adopt a simple linear regression model. Table 4 describes the explanatory and dependent variables included in the model. The dependent variable is the average (annual) OECD inflation rate. When computing the average, we use individual inflation rates weighted by corresponding real GDPs. Based on the result of the PCA in Section 2 and the results of Ciccarelli and Mojon (2010), both the first principal component and the OECD inflation rate can be interpreted as a global inflation factor. Because most explanatory variables are only observed annually, the annual OECD inflation rate is used instead of the first principal component estimated with quarterly data in Section 2.

Note: The variable collection corresponds to the suggestion of Ravn and Uhlig (2002).

Source: OECD; Data period: 1981 to 2016.

The first explanatory variable represents the aggregate labor supply of OECD countries. The second explanatory variable represents the indicator of the internal trade importance. The third variable presents the monetary policy in OECD countries. The fourth and fifth variables indicate the aggregate production activity in OECD countries. The last variable is the global oil price, which is an important production factor. The two variables for the OECD economic activity participation rate and the OECD trade volume are observed annually. Thus, the observations of the other explanatory variables are adjusted to an annual frequency. The empirical data begin from 1981 because the aggregate OECD currency volume (M2) has been reported since 1981.

Table 5 shows the ordinary least squares (OLS) estimates based on the data from 1995 to 2016. To avoid the multicollinearity problem, only one of the two variables that represent production activity (OECD Industrial Production Index and OECD Real GDP Cycle) is included in the model. Of the five explanatory variables, only two are statistically significant. The most important variable is the OECD M2 growth rate, which represents the monetary policy. As shown in Table 5, the estimated coefficient for the OECD M2 growth rate is statistically significant at the 1% significance level. Additionally, the absolute value of the estimate is highest among all of the other estimated coefficients. This result is in line with economic theory.

Note: ***: 1% statistical significance, **: 5% statistical significance, *: 10% statistical significance.

The second most important explanatory variable is the trade/GDP ratio. An increase in the trade/GDP ratio can be seen as a sign of global trade liberalization. A study by Melitz and Ottaviano (2008) theoretically shows that trade liberalization triggers commodity competition and as a result lowers the price levels of many countries. They also provide empirical evidence for the theoretical prediction. Other variables can be interpreted, but their estimated coefficients are not statistically significant. Thus, I omit them here.

For a robustness check, the sample period is extended to from 1981 to 2016. As before, the M2 growth rate and the trade/GDP ratio are statistically significant at the 1% significance level. The Dubai oil price is a statistically significant variable at the 10% significance level only when using the recent sample from 1995 to 2016.

Because variables of the same year are used in the regression model, one may be concerned about reverse causality. Therefore, Table 6 reports the result of a model with one-year lagged explanatory variables. The new model with the lagged values of the explanatory variables produces no meaningful change in the estimated coefficients. Furthermore, the result is robust if the OECD Industrial Production Index is used instead of the OECD Real GDP Cycle (OECD Real GDP Cycle results are not reported here).

Note: ***: 1% statistical significance, **: 5% statistical significance, *: 10% statistical significance.

It is consistent with the traditional theory that an increase in M2 in OECD countries leads to an increase in global inflation. The central banks of many countries have been aggressively using expansionary monetary policy instruments since the 2008 financial crisis. The monetary policy stance has been maintained for more than ten years in the EU and Japan. While as of 2019, the Federal Reserve Bank (Fed) moved from an expansionary policy and started to tighten their balance sheet, many experts expected that the tightening monetary policy cannot last long due to signs of an economic recession.

It is difficult to find a reasonable explanation for the globally low inflation for recent years. For example, from 2012 to 2016, many developed countries experienced low inflation despite the use of aggressive expansionary monetary policies. During most of the time period, actual inflation rates were lower than the corresponding inflation targets.

This study suggests that the rapid growth in international trade is an important driver of the low global inflation. Figure 13 shows the explained part of the OECD inflation rate according to the OECD M2 growth rate. The long-term inflation trend looks similar to the OECD M2 growth trend. However, since the mid-1990s, the OECD inflation rate has declined more rapidly than what the OECD M2 growth suggests.

Note: The vertical axis on the left represents the unit of the OECD inflation rate, and the vertical axis on the right represents the unit of the product of the rate of increase in the amount of currency in the OECD and the corresponding coefficient.

Figure 14 plots the unexplained part of the OECD inflation rate according to OECD M2 growth along with the OECD trade/GDP ratio. In the mid-1990s, the OECD trade/GDP ratio dramatically increases. Although China is not a member of OECD, this trend is very similar to China's growth in trade volume since the opening of their economy. Figure 14 shows that the OECD trade/GDP ratio inversely moves together with the unexplained part of the OECD inflation rate. The sharp increase in international trade is linked to global trade liberalization. Melitz and Ottaviano (2008) theoretically show that trade liberalization can trigger product competition and can lower the aggregate price level of a country. The result in Figure 14 provides evidence of this theoretical prediction.

Note: The vertical axis on the left represents the unit for the residual term, where the rate of increase in the amount of OECD currency in OECD inflation is eliminated, and the vertical axis on the right represents the unit for trade against the OECD GDP.

The U.S. government has attempted to resolve the long-lasting trade imbalance with China by imposing high tariffs. Many scholars and policymakers believe that such trade barriers can decrease the aggregate trade volume in the global economy. The aforementioned result predicts that a sharp decrease in international trade can exert strong inflation pressure on many countries in the long-term.

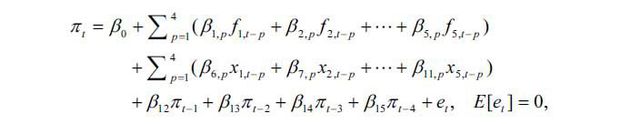

For a quantitative analysis, this study considers the first five principal components estimated in the previous section and six macro-variables in a linear regression model:

where et represents the residual term of the linear regression model. The dependent variable is the QoQ Korea CPI inflation rate. For each variable, including the dependent variable, four lagged values are used as additional explanatory variables.1

The macro-variables in the model are explained in detail in Table 7. Domestic macro-variables for the Korean economy included in the model represent the domestic monetary policy, production activity, labor market, and exchange rate. The international macro-variable included in the model is the Dubai oil price. Including the lagged Korea inflation rates, in total 44 explanatory variables are used in the model. The main sample period is from the second quarter of 1998 to the second quarter of 2018, and only quarterly data are used in the analysis. The beginning period is determined by considering the time when the bank of Korea’s inflation targeting began.

Note: The vertical axis on the left represents the unit for the residual term, where the rate of increase in the amount of OECD currency in OECD inflation is eliminated, and the vertical axis on the right represents the unit for trade against the OECD GDP.

Source: Bank of Korea, Period: 1975:Q1~.

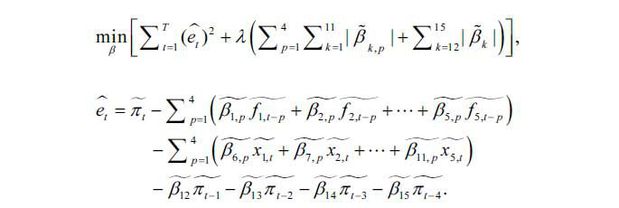

In the sample, there are only 81 observations. This means that only two observations can be used to estimate one coefficient in the model. Therefore, reasonable statistical inference is not possible with the standard OLS method. Moreover, even if a researcher attempts to reduce the number of variables in the model by excluding unnecessary variables, there are tens of thousands of models that can be constructed from a subset of 44 variables. In this context, choosing an optimal model could be a very difficult task. This study adopts a big data technique, the LASSO (Least Absolute Shrinkage and Selection Operator) method, for model selection.2

The LASSO method minimizes the following objective function:

In the equation above, λ is a penalty parameter that is set by the researcher. If the OLS estimate of a coefficient for an explanatory variable is close to 0, this penalty term forces the estimated coefficient value to be exactly 0 and automatically estimates the model after excluding the corresponding variable. In the opposite case, if the OLS estimate of a coefficient is significantly different from zero, the penalty term does not greatly affect the estimated value of the coefficient. That is, the LASSO method divides the entire set of explanatory variables into two groups: one group composed of variables with zero coefficients and the other group composed of variables with non-zero coefficients. If the standard OLS method is applied to the model while excluding variables with zero coefficients, the final estimation result would be very similar to that obtained by LASSO.

All of the explanatory variables are normalized using their sample means and standard deviations before applying the LASSO method such that the means and standard deviations of the normalized variables are zero and one, respectively. In the equation above, the upper bar attached to each variable and coefficient means that the corresponding variable is normalized before the estimation. This normalization ensures that the effect of the penalty term on each variable is not affected by the variable’s mean or standard deviation.

In the LASSO method, variable selection or model selection depends on the penalty parameter λ. For instance, if the value of λ is large, LASSO does not include any variables in the model. Conversely, if the value of λ is close to 0, all variables are included in the model. Therefore, by changing the value of λ from a very large value to a small value, one can easily check which variables have significant effects on a target dependent variable.

Table 8 shows which variables are selected by LASSO for the Korean inflation rate. The first selected variables are the first and third principal components. Next, the third lagged Korean inflation rate is included, followed by the Korean call rate. Korea's M2 growth rate and the second principal component are also selected next. Note that the principal components are estimated while excluding the Korean inflation rate to avoid using the same data information twice.

Figure 15 shows how the LASSO estimates change depending on the value of λ. As explained above, the LASSO estimates deviate from 0 as the value of λ decreases. The variables selected by LASSO are mostly statistically significant, but these estimates may not be easy to interpret economically because all variables are normalized before the estimation. In order to assess the actual relationships between the explanatory variables and the Korean inflation rate, OLS estimation is performed without the normalization step using the eight variables selected by LASSO in Table 8.

Table 9 shows the result of the OLS estimation. The OLS estimate indicates that the selected principal components with different lagged orders suitably explain the short-term movements of the Korean inflation rate. In particular, one quarter of the lagged principal components have significant effects on the Korean inflation rate. Among many macro-variables, Korea's M2 growth rate is found to be statistically significant. Indeed, in Table 9, most of the variables selected by LASSO are statistically significant, except the three-quarter lagged call rate. According to the R-squared outcome, the selected variables account for 62% of Korea's inflation rate for last 20 years.

The previous section employs LASSO to select important variables that explain Korean inflation. However, due to the limited amount of the data, various statistical errors and issues may occur. Moreover, the statistically significant variables in the in-sample estimation may not provide strong predictive power. Thus, it is necessary to evaluate whether the selected variables can predict the future inflation rate. The prediction performance is evaluated using the sample from the fourth quarter of 2007 to the second quarter of 2018, a period which includes the financial crisis period. The weights that are used to construct the principal components are estimated prior to the fourth quarter of 2007 and are fixed through the prediction period.

The evaluation for the forecast is summarized in Table 10. Model 1 assumes that the Korean inflation rate follows a random walk process. The model implies that the optimal forecast for the next quarter is the current inflation rate. The random walk model is treated as a benchmark model in this section.

Model 2 is an AR(4) model that uses four lagged values of the dependent variable as explanatory variables. Models 3 to Model 10 all are AR(4) models with each explanatory variable in Table 7. Four lagged values of each explanatory variable are included in the models. Model 11 includes Korea's M2 growth rate and real GDP growth rate, which are known to be important when explaining the dynamics of the Korean inflation rate. Model 12 includes only the variables selected by LASSO in the previous section. Model 13 uses the OECD inflation rate and China’s inflation rate to replace the first three principal components, reflecting the result of Section 3. For the prediction analysis, it is assumed that relevant variables are known prior to the prediction and that they are identified by LASSO. This may be a limitation in that the LASSO estimation uses the full sample. However, it is a necessary assumption because the full sample size is already relatively small compared to the number of parameters.

Table 11 shows the mean squared error (MSE) for each model along with how much the MSE of each model deviates from that of the benchmark random walk model (Model 1) in terms of the percentage. The main result is that all models except Model 12 and Model 13 show worse predictive performance than the random walk model. On the other hand, Model 12 reduces the MSE by about 30% compared to Model 1. Similarly, Model 13 reduces the MSE by about 11% compared to Model 1.

Note: The MSE difference in percentage between Model 1 and a comparison model is shown in parentheses.

Source: Estimates - author’s calculations.

To test for whether the improved predictive power over the benchmark model is statistically significant, the predictive hypothesis test of Clark and West (2007) is utilized. In the hypothesis test by Clark and West (2007), the null hypothesis assumes that a compared model and the random walk model have the same predictive power. The alternative hypothesis assumes that a compared model has better predictive power than the random walk model. Table 12 reports the test statistics for Models 12 and 13. For both models, the improvement in the prediction is statistically significant at the 1% significance level.

Note: 1) ***: 1% statistical significance, **: 5% statistical significance, 2) 1% critical value: 1.28, 5% critical value: 1.645.

It is easy to infer based on the hypothesis test result that the principal components or the global inflation factors play a very important role in the prediction. Note that the out-of-sample forecast is not improved by any of the models that include only Korean domestic macro-variables or the oil price. Only the models that include the principal components (or OECD and China’s inflation rates) and macro-variables selected by LASSO greatly improve the prediction performance. This is consistent with the in-sample analysis, where all of the first three principal components are statistically significant.

Section 2 shows that the first principal component is nearly identical to the OECD inflation rate. Therefore, the first principal component can be interpreted as a global inflation factor, as documented by many previous studies. This study also shows that the global inflation factor is closely related to the OECD M2 growth rate and the OECD trade/GDP ratio. Another important empirical implication from Section 2 is that the second and third principal components reflect information about China’s inflation rate.

The empirical analysis in this section offers us evidence that global inflation synchronization, which is potentially reflected in the principal components, has a profound effect on the Korea inflation rate in the short-term. If one needs to predict the Korean inflation rate in the short-term, the common variations in many countries’ inflation rates (their lagged values) will provide valuable information.

This section extends the analysis in the previous section by considering the range from one-year to two-year forecasting periods. That is, this section focuses on predicting how much the aggregate price level in Korea will change after one or two years from the present. For the one-year-ahead (or two-years-ahead) prediction, we use the one-year (or two-year) inflation rate as the target dependent variable. When computing the mid-term inflation rates, much of the short-term movement in the aggregate price will be eliminated. Thus, only mid-term economic factors that affect inflation for more than one year will be reflected in the observed inflation rate. Finding these factors is the main objective of this section.

All models described in Table 10 are used for the predictive performance evaluation. For the explanatory variables, their annual growth rates or annual averages are used instead of the quarterly growth rates or the quarterly averages. Only the one-year lagged values of the dependent variable and the explanatory variables instead of four lagged values are included in the models. LASSO selects the first three principal components, the call rate, and the annual M2 growth rate in the in-sample estimation. All variables are included in Model 12. As before, Model 13 replaces the first three principal components with the OECD and China’s inflation rates.

The prediction result is reported in Table 13. We find that models with the real GDP growth rate show better predictive power than the benchmark random walk model (Model 1). The model with the real GDP growth rate (Model 8) shows that the MSE decreases by about 42% compared to Model 1. Model 11 contains both the real GDP growth rate and the M2 growth rate. When these two variables are used together, the predictive power is further improved than when each variable is used separately. The model with the KRW / USD exchange rate (Model 9) and the model with the Dubai oil price (Model 10) also exhibit less predictive power than the models that contain the real GDP growth rate and the M2 growth rate. The change in the set of important variables compared to the previous section can be attributed to the fact that short-term inflation movements are largely eliminated when calculating the one-year inflation rate.

Note: The MSE difference in percentage between Model 1 and a comparing model is shown in parentheses.

Source: Estimates - author’s calculations.

Note: The MSE difference in percentage between Model 1 and a compared model is shown in parentheses.

Source: Estimates - author’s calculations.

Finally, we perform an out-of-sample predictive analysis for the two-year-ahead inflation rate. Similar to the one-year-ahead prediction, Model 11's predictive power is the highest. To investigate the predictive power of Model 11 further, the statistics of Clark and West (2007) are computed and reported in Table 15. The result shows that the improved predictive power of Model 11 is statistically significant at the 1% (5%) significance level for the one-year (two-year) prediction case.

The previous sections provide quantitative analyses to examine whether the principal components of inflation suitably explain or predict short- and mid-term movements of the inflation rate in Korea. This section presents policy implications based on the reported results thus far.

The important empirical results of the PCA are summarized as follows. The first principal component can be interpreted as the global inflation factor documented by studies such as those by Ciccarelli and Mojon (2010) and Mumtaz and Surico (2012) because the estimated first principal component shows movements nearly identical to those of the OECD inflation rate. By looking at several OECD macro-variables, we find that the OECD inflation rate is largely determined by two factors: the M2 growth rate for OECD countries and the OECD trade/GDP ratio. Section 3 shows that the Korean inflation rate is directly affected by the first principal component or the OECD inflation rate. In particular, we can infer that the OECD inflation rate acts as a short-term driver of Korea’s inflation because it predicts Korea’s inflation rate one quarter ahead. In addition, the second and third principal components, which are directly related to China’s inflation rate, have significant in-sample explanatory power for Korea’s inflation rate in the short-term. However, the performance outcomes of the principal components for the one-year- and two-year-ahead predictions are not satisfying.

It is shown in Figure 1 and Figure 2 that Korea's inflation rate changes almost simultaneously with those of the developed countries. Figure 16 indicates that China's quarterly inflation rate tends to move one or two quarters ahead of Korea’s quarterly inflation rate. In particular, this phenomenon is observed for about five years before and after the 2008 financial crisis. Figure 17 compares Korea’s and China’s yearly inflation rates. The pointed pattern seems clearer in the yearly data. This would be other evidence suggesting that China's inflation rate can be used to explain or predict Korea’s inflation in the short-term.

The rapid increase in the trade volume between Korea and China over the last 30 years has triggered strong inflation coordination. In addition, the cheap labor and scale production of the Chinese economy appear to play an important role in reducing the prices of many Chinese products which are exported to Korea. Because China’s inflation is directly related to the low production cost and Chinese products are exported to Korea, it is reasonable to conjecture that China’s inflation precedes Korea’s inflation. This is also consistent with the evidence that one of the main determinants of OECD inflation is the OECD trade/GDP ratio.

Many studies mentioned in the previous sections argue that the short-term and mid-term movements of inflation in each country are mainly determined by a single global inflation factor. As a result, they conclude that the global low inflation phenomenon is attributed to the low global factor, which is independent of domestic monetary policies. However, this study provides evidence that more than one global factor and their corresponding effects on the Korean inflation rate are limited in the mid-term, despite the fact that these effects are non-negligible in the short-term. Another important finding of this study is that the mid-term trend of Korea’s inflation is largely determined by the monetary policy of the Bank of Korea and the Korean economic situations in that Korea’s domestic macro-variables well predict its inflation rate ahead by one or two years.

Since 1998, the Bank of Korea's policy goal has been to promote price stability via inflation targeting. It is well known that a monetary policy affects the economy with some lags. Previous studies such as those by Lee et al. (2005) and Kim (2010) argue that Korea’s monetary policy has somewhat faster effects on the economy compared to other developed countries and that these effects last for more than a year. The characteristics of Korea’s monetary policy imply that the Bank of Korea should determine the proper direction and timing of their monetary policy instruments only after carefully considering both short-term and the mid-term effects. This also requires good predictions of future inflation rates. Overall, our main empirical results suggest that the Bank of Korea should implement monetary policy in line with domestic economic conditions which have dominant mid-term effects rather than global inflation factors which have only short-term effects. In addition, in the light of the result that China’s inflation rate precedes Korea’s inflation rate, China’s inflation rate would be a good candidate variable for policymakers to forecast Korea’s inflation rate more accurately.

As of 2019, the central bank of the United States has maintained a tightening monetary policy and the U.S. inflation rate has remained close to the target rate 2%. However, at that time, there were many factors that could lead to a decline in inflation. Even before the coronavirus pandemic, the short- and long-term interest rates were reversed, which is a strong sign of an economic recession. Moreover, due to the trade dispute with China, positive outlooks for the global economy are difficult to find. In Europe, many experts noted that a sharp increase in government debt could have a strong adverse effect on the economy. Now, the coronavirus pandemic is aggressively suppressing aggregate demand. Despite the fact that the trade dispute between the US and China will have a negative impact on the global trade volume, which will create upward pressure on inflation, it appears to be more convincing that global inflation will undergo strong downward pressure in the long-run considering the global virus pandemic, which dampens both global demand and supply. We leave the effects of the virus pandemic on global and Korea inflation as an important future research agenda.

This study analyzes the recent global inflation synchronization and examines its policy implications for the Korean economy. Unlike previous studies that emphasize the importance of a single global inflation factor, it is shown here that more than one global inflation factor affect Korean inflation in the short-term, while their mid-term impacts are limited. The Bank of Korea’s 2018 monetary credit policy report indicates that the link between domestic inflation and global inflation in the Korean economy has shown a rapid rise since the 2008 financial crisis. On the other hand, Kamber and Wong (2018)’s International Settlement Bank (BIS) report argues that the impact of the global inflation factor on a country’s inflation lasts only in the short-term, while its long-term inflation trend is determined by the county’s monetary policy stance. Regarding the important question of whether domestic inflation has become a slave to global inflation factors or whether domestic monetary policy remains a valid policy instrument, this study provides important policy implications consistent with Kamber and Wong (2018). However, this does not necessarily intend to ignore the effects of the global inflation on the Korean inflation rate in the mid-term or long-term. Rather, it means that many domestic macro-variables well reflect global macro environments over time. Therefore, it is desirable to pay close attention to domestic macro-variables when enacting monetary policy.

This paper is based on Sora Chon, 2018, International Inflation Synchronization and the Implications, Policy Study 2018-07, KDI (in Korean). Valuable comments by two anonymous referees are appreciated.

A variable having predictive power does not necessarily mean that the variable has a definite causal effect on the dependent variable. In order for the interpretation to hold, we must make a couple of assumptions. The first is that in the empirical model, some of the variations for Korea’s inflation rate that are derived by domestic macro-shocks are well controlled by lagged domestic macro-variables. The error term in the model will then be a combination of domestic and global shocks. If a global shock persistently affects a global factor and the global factor affects the Korean inflation rate, the lagged values of the global factor will have predictive power. Thus, the predictive power is indirect evidence of a causal effect under these assumptions. This study implicitly uses these assumptions.

, , & . (2015). Understanding the great recession. American Economic Journal: Macroeconomics, 7(1), 110-167, https://doi.org/10.1257/mac.20140104.

, & . (2010). Global inflation. The Review of Economics and Statistics, 92(3), 524-535, https://doi.org/10.1162/REST_a_00008.

, & (2007). Approximately normal tests for equal predictive accuracy in nested models. Journal of econometrics, 138(1), 291-311, https://doi.org/10.1016/j.jeconom.2006.05.023.

. (2009). Implementing Horn's parallel analysis for principal component analysis and factor analysis. The Stata Journal, 9(2), 291-298, https://doi.org/10.1177/1536867X0900900207.

, & (2019). Deterministic parallel analysis: an improved method for selecting factors and principal components. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 81(1), 163-183, https://doi.org/10.1111/rssb.12301.

. (2011). The long slump. American Economic Review, 101(2), 431-469, https://doi.org/10.1257/aer.101.2.431.

(1965). A rationale and test for the number of factors in factor analysis. Psychometrika, 30(2), 179-185, https://doi.org/10.1007/BF02289447.

Ottaviano & (2008). Market size, trade, and productivity. The review of economic studies, 75(1), 295-316, https://doi.org/10.1111/j.1467-937X.2007.00463.x.

, & . (2012). Evolving international inflation dynamics: world and country-specific factors. Journal of the European Economic Association, 10(4), 716-734, https://doi.org/10.1111/j.1542-4774.2012.01068.x.

(2000). SPSS and SAS programs for determining the number of components using parallel analysis and Velicer’s MAP test. Behavior research methods, instruments, & computers, 32(3), 396-402, https://doi.org/10.3758/BF03200807.

OECD. OECD, https://data.oecd.org/price/inflation-cpi.htm, accessed: 15 October 2018.

, & . (2002). On adjusting the Hodrick-Prescott filter for the frequency of observations. Review of economics and statistics, 84(2), 371-376, https://doi.org/10.1162/003465302317411604.

The Bank of Korea. The Bank of Korea, https://ecos.bok.or.kr/, accessed: 15 October 2018.

World Bank. World Bank, https://data.worldbank.org/, accessed: October 15, 2018.