- P-ISSN 2586-2995

- E-ISSN 2586-4130

This paper aims to identify the most effective mode of development finance flows for the economic growth of middle-income developing and least developed countries, separately. It also attempts to confirm whether governance has any significant role in the causal relationship between development finance flows and economic growth. Policymakers in each developing country should select the most effective modality of development finance inflows among the different modalities (such as Official Development Assistance (ODA) grants, Official Development Assistance (ODA) loans, FDI, and international personal remittances) and expand it for their economic growth. Dynamic panel regression models were used on 48 least developed countries and 89 middle-income developing countries, respectively, during the Millennium Development Era: 2000-2015. The empirical analysis results show that ODA grants and remittances were most effective in promoting economic growth for least developed countries, while FDI was most effective for middle-income developing countries. These findings were not affected by the status of governance of the individual country.

ODA Grants, ODA Loans, FDI, Remittances, Economic Growth, Least Developed Countries, Effectiveness, Middle-income Developing Countries

C36, F24, G15, O11, P45

This paper aims to identify the most effective mode of development finance flows for the economic growth of middle-income developing and least developed countries, separately. Policymakers in developing countries should select the most effective modality of development finance flows and expand it for the economic growth of developing countries.

Mainstream development economists have emphasized that growth cannot take place in the absence of capital. In the absence of technical progress, output growth is limited by the rates of capital formation and population growth. In relatively labor-abundant developing countries, this implies that capital shortages constrain growth given that national income is lower; therefore, savings and investment rates are lower. Naturally, many development economists have advised policymakers in developing countries to attract foreign savings or development finance flows from advanced countries. This helps to resolve another critical constraint on development, i.e., foreign exchange shortages.

However, selecting the most effective mode of development finance flows has proved challenging for developing countries. FDI (foreign direct investment) has been criticized for having negative social side effects and for its concentration on rapidly growing emerging economies; concessional and non-concessional loans have been criticized for their debt accumulation effects, while ODA (official development assistance) grants have been criticized for their tendency to induce corruption and their fungibility with regard to domestic resources; and international remittances have been limited by advanced countries’ regulations on immigration and remittances. (The category known as Other Official Flows (OOF) is not explicitly dealt with in this study owing to its relatively small size and nondevelopment assistance characteristics.)

Moreover, concerns have been expressed over the adequacy of development finance flows. On the supply side, private capital flows towards developing countries experienced an abrupt decline in the middle of 2008. After a short recovery, net private capital flows to developing countries still exhibit a downward trend (IMF: World Economic Outlook 2016). On the demand side, the financial resources required to implement the SDGs (sustainable development goals) for the period ending 2030 are so enormous and amorphous that a reasonable estimate of the demand has not yet been agreed upon (Martin and Walker, 2015). Policymakers of developing countries will not only have to prioritize their investment priorities but also must take a strategic approach in accessing different types of development finance flows.

The need to assess the relative effectiveness of the different types of development finance flows is also accentuated by the converging trend of the different types of development finance inflows selected by developing countries in recent years, although the relative sizes of those finance flows have varied in the past (Figures 1 and 2). Since 2004, capital inflows to developing countries have been largely dominated by FDI. However, recently all four types of development finance which have flowed into developing countries (FDI, remittances, private debt and portfolio and ODA flows) have shown a tendency to converge (Figure 1). Since 2002, the number of developing countries, which favored a certain type of foreign capital flows most, has been tending toward four types of capital inflows (Figure 2). This tendency naturally raises the question of whether developing countries find that all four types of development finance flows are equally conducive to their economic growth and thus find themselves indifferent to their roles in economic growth.

Source: World Bank Group (2017).

Source: Mulakala (2017).

The process and stage of development and industrialization of an economy do matter when establishing the relative priorities of foreign capital inflows for accelerating economic growth in developing countries. When writing this paper, we deemed it necessary to investigate at least two groups of countries at different development stages, i.e. middle-income developing and least developed countries, and examine which mode of foreign capital inflows has the most favorable effect on growth for each group.

Furthermore, the existing empirical literature is ambiguous as to whether foreign aid or ODA promotes economic growth in recipient countries, and it provides widely divergent estimates of the cross-country relationship between foreign aid inflows and economic growth rates. However, earlier studies have one common characteristic: they all examined the impact of aggregate aid on growth. Not all aid, however, affects growth similarly, and types may vary depending on the motives, purposes, donors, and characteristics of the aid (Akramov, 2012). Therefore, an increasingly popular direction in the literature is to examine the impact of disaggregated aid on developmental outcomes (Clemens et al., 2004; Dreher, Nunnenkamp and Thiele, 2008; Mishra and Newhouse, 2009; Birchler and Michaelowa, 2016). Thus, this study builds on the recent attempts to investigate whether different types of aid (i.e., grants and loans) influence the effectiveness of the aid in promoting economic growth.

Moreover, in the literature pertaining to the effectiveness of aid, one of the most controversial findings was that “good policy and/or an institutional environment” will determine the effectiveness of aid on economic growth. Aid has a statistically significant positive effect on economic growth, mainly in aid-recipient countries with good policies and institutional environments, but it is limited in those with poor policies and poor institutional environments (Burnside and Dollar, 2000; Collier and Dollar, 2002). Similar findings were also reported with respect to the effectiveness of FDI and international remittances. Therefore, when comparing the effectiveness of different types of development finance flows into developing countries, it is important to control for the effect of the quality of policies and institutions.

Specifically, the research questions of this study are as follows:

Which type of external capital inflow has the most significant impact on the economic growth of middle-income developing countries and least developed countries, separately?

How important is the governance of middle-income developing countries and least developed countries for foreign capital inflows to have positive effects on economic growth?

Based on the limited availability of private capital inflows for least developed countries and their low level of economic and political governance and capacity relative to those of middle-income developing countries, we presume that ODA will more likely have a greater impact on economic growth for least developed countries. In contrast, for middle-income developing countries, which are equipped with relatively better economic and political institutions and infrastructures for investment compared to those of least developed countries, private capital inflows such as FDI will have a more significant impact on economic growth.

In carrying out empirical tests on the research questions presented above, dynamic panel regression models were used on 48 least developed countries (with 2015 per capita GDP<$1,025, following the World Bank classification) and 89 middle-income developing countries (per capita GDP: $1,026 - $12,475) during the Millennium Development Era, i.e., from 2000 to 2015. All data were collected from the World Bank Development Indicators of the World Bank.

This study is structured as follows. The following section reviews the literature on the topic. Section 3 provides a detailed description of the methodology and data used in this study. Section 4 analyzes the empirical results, and section 5 summarizes the key findings and derives policy implications with suggestions for future research.

We will review the existing literature on the effectiveness of foreign capital inflows for economic growth in developing countries. Initially we review the literature on the effectiveness of official development assistance (ODA), after which we examine the scholarship on the effectiveness of private capital inflows.

The overall body of literature can be divided into four groups. The first holds that aid is ineffective in almost all cases. Second, aid is, on average, effective only with decreasing returns. Third, aid is ineffective in general but effective when the economic management policies and/or political and economic institutions of the aid-recipient countries are good. Lastly, different components of aid show disparate degrees of effectiveness.

These studies represent the conventional views expressed by Bauer (1976); Friedman (1995); Boone (1996); Easterly, Levine, and Roadman (2004); and Rajan and Subramanian (2008). Their results show no significant positive or negative relationship. Furthermore, some in this group even argue that aid is potentially counterproductive as it helps expand bureaucratic organizations or helps make them inefficient; enriches the elite class or special interest groups; sustains corrupt regimes, causing Dutch disease in aid-receiving countries; reduces farmers' incomes by lowering the prices of agricultural products; promotes the interests of donor governments, their enterprises, or interest groups; and encourages any positive effects to disappear into unproductive government consumption, adversely affecting legal and economic institutions (Remmer, 2004; Rajan and Subramanian, 2005; 2007; Heckelman and Knack, 2008).

The research results of the economists belonging to this group show that although aid does not have the same effects everywhere and that it does have, on average, a positive impact on growth. According to this group, aid does stimulate investment or enhance long-term productivity when foreign aid is modeled as an exogenous transfer of income or capital to recipient countries, and foreign aid has only decreasing returns. Therefore, as the amount of aid increases, the effects of the aid on growth would rise at a decreasing rate. Many IMF economists have argued along these lines since the 1990s (Cassen, 1994; Dalgaard, Hansen, and Tarp 2004; Arndt, Jones, and Tarp, 2010).

This group includes research results that show that aid has been effective in promoting growth only when aid recipients meet certain conditions. Such conditions have been advanced mostly by World Bank economists either as good political institutions, i.e. democracy or civil liberty (Isham, Kaufmann, and Pritchett, 1995; Kosack, 2003) or good economic institutions and policies (World Bank, 1998; Burnside and Dollar, 2000; Collier and Dollar, 2002).

One of the increasingly popular directions in the literature is to examine the impact of disaggregated aid on development outcomes (Akramov, 2012). Official development assistance (ODA) is largely divided into grants and loans depending on whether repayment of the loan is required or not. Lerrick and Meltzer (2002) claimed that grants are preferable to loans in making aid programs effective and preventing the accumulation of unpayable debt. Cordella and Ulku (2007) also find that grants prove effective only in highly indebted poor countries with bad policies, as grants imply fewer repayment obligations, though there are also fewer resources available for donors to provide to recipients. A study by Clemens et al. (2004), disaggregating aid by sector, finds that only “direct aid,” which is used for building infrastructure (e.g., roads, irrigation, power, ports) and for enhancing productive sectors such as agriculture and industry, stimulates economic activities over a four–year period (“short-impact aid,” about 53% of all ODA flows recently) and that it has strong positive and causal effects on economic growth, albeit showing diminishing returns. “Indirect aid” for the human resource development (i.e., education and health), governance, and environmental sectors contributes to economic growth only over longer periods. Mishra and Newhouse (2009) reveal a small but statistically significant effect of health aid on infant mortality. Similarly, Dreher, Nunnenkamp, and Thiele (2008) find that a higher level of per capita aid for education has a statistically significant positive impact on primary school enrollment rates; recently Birchler and Michaelowa (2016) present a similar finding. Furthermore, Lee and Lee (2014) show that different types of aid (grants vs. loans) result in different public finance management responses from recipient governments, and Rugare and Lee (2016) demonstrate that different delivery modes of aid (project aid vs. program aid) lead to disparate effects on the percapita income growth of aid recipient countries in Sub-Saharan Africa.

The fundamental proposition of this disaggregated aid effectiveness approach is that different aid components may have different transmission channels with regard to their impact on economic growth. Moreover, ODA plays an instrumental role in development financing, particularly in countries with a limited capacity to attract private direct investment (United Nations, 2002). Most if not all of these countries are in the group of least developed countries, highly devoid of features that would attract foreign private investment. Thus, for least developed countries, the relatively steady and easily available external finance source of ODA can play a pivotal role in building necessary infrastructure, which may then help attract foreign private resources for further investment. In contrast, middle-income developing countries, especially emerging development countries, can be relatively more capable of repaying loans and have easier access to loans, foreign direct investment, and international remittances.

A serious problem with many of these studies as reviewed above is that they concentrated on a single group of developing countries with a similar per-capita income level. In this study, therefore, we will examine whether countries at different stages of development show disparate impacts of foreign capital inflows, specifically both middle-income developing countries and least developed countries.

Consequently, in this study, we will disaggregate total aid into grants and loans and will analyze their impacts on the economic growth of developing countries at different stages of development (middle-income developing countries vs. least developed countries). This leads to our first hypothesis:

Private capital generally consists of foreign direct investment (FDI), portfolio investments, and international remittances. However, under the judgment that portfolio investment constitutes a scant proportion of total developmental capital inflows for least developed countries, while remittances are perceived as significant private earnings for many households, we take into account remittances but exclude portfolio investments in this study.

FDI, a type of investment made by a company based in one country in a company based in other developing countries in this study, has shown mixed effects in the literature. Findlay (1978) asserted that FDI increased the rate of technical progress in the host country through a “contagion effect” emanating from the advanced technology and management practices used by foreign firms. Further evidence of the effect of FDI on economic growth in Latin America was provided by De Gregorio (1992), who stated that the increased growth from FDI was three times greater than that by domestic investment.

Other scholars challenged the positive effect of FDI, arguing that FDI crowds out domestic investment (Fry, 1993) and has limited or no effects on industrial growth in developing countries (Singh, 1988). Mencinger (2003) highlighted the adverse effect of FDI in developing countries, where it can force small emerging local competitors out of business, with multinationals paradoxically contributing more to imports than exports.

Still others showed that FDI proved effective only under certain circumstances. The effectiveness of FDI prevails when the host country has a minimum threshold stock of human capital (Borensztein, 1995). Borensztein et al. (1998) investigated the effect of FDI on the economic growth of developing countries using panel data over two decades, concluding that human capital development is crucial for a country to benefit from FDI inflows. Blomstrom and Kokko (2001) demonstrated that FDI is not effective for lower income developing countries, as they lack the technological level and capacity to imitate foreign invested firms, and their poor business environments may lead to insignificant or even detrimental outcomes (Bruno and Campos, 2011).

Considering the dependent feature of FDI on the economic condition of recipient countries, the high political instability and poor infrastructures in least developed countries, and clearly the limited amount of FDI, we presume that FDI is ineffective in promoting economic growth in least developed countries.

This leads to our second hypothesis:

Regarding the effectiveness of international personal remittances transferred by migrant workers to their countries of origin, Giuliano and Ruiz-Arranz (2009) hold an optimistic view, corroborating it with an empirical analysis showing that remittances promote growth in countries with underdeveloped financial systems by offering an alternative means to finance investment and ease liquidity constraints. Gupta, Pattillo, and Wagh (2009) suggest that remittances have a direct impact on reducing poverty and promoting financial development. Their bottom line statement is that remittances offer unbanked small-saver households the opportunity to access the formal financial sector.

However, Chami, Fullenkamp, and Jahjah (2003), taking an opposing stance, developed a unified model to examine the causes and effects of remittances on an economy. They concluded that a moral hazard problem that arises between remitters and recipients, under asymmetric information and a lack of observability of the recipients’ actions, had a negative impact on economic growth. Their explanation is that recipients’ dependency on remittances will reduce the supply of labor.

On balance, previous studies focused narrowly on the impact of a single type of capital inflow on the economy, and they paid insufficient attention to least developed countries. A comparative study by Benmamoun and Lehnert (2013), who examined the effects of FDI, ODA, and international remittances, shows a significant positive impact from all three types of capital inflows on low-income countries, finding that international remittances have dominant effects over the two other types of capital flows. However, their study shows no significant impact of any of the three types of capital inflows on middle-income developing countries. Moreover, governance has significant positive effects on national income growth for low-income countries but shows significant negative effects on national income growth for middle-income countries. In general, governance in middle-income countries is superior to that in low-income countries. Such contradictory and incomprehensible statistical results may be due to the misspecification of the estimation model. Since 1960, it has been well known that economic growth can be promoted not only by investment in physical capital but also by investment in human capital (Schultz, 1961). However, the estimation model of Benmamoun and Lehnert (2013) lacks both investments in physical and in human capital. Such missing variables may have led to the mixed and incomprehensible results.

Therefore, we intend to include in our estimation model investments in both physical and human capital, as well as governance interacting with the three different types of capital inflows. In this way, we are able to preclude bias due to missing variables and know whether governance plays any significant role through interactions with any type of capital inflows. In other words, certain types of capital inflows by themselves may not statistically significantly influence the growth of national income but may be statistically significant if they interact with the good governance of the country in question, as Burnside and Dollar (2000) and Collier and Dollar (2002) show the effectiveness of ODA in promoting the economic growth of recipient countries. This has led us to test a third hypothesis:

H3:

The different types of development finance flows would become effective only when the governance of recipient developing countries is sound or reformed.

Another recent comparative study of the effectiveness of different types of development finance flows (Driffield and Jones, 2013) did incorporate both human capital and governance in the estimation model. However, the authors of that study also used aggregate ODA for all developing countries in their analysis, assuming that all developing countries, irrespective of their development level, would face the same problems with respect to development finance inflows and therefore would need the same strategy regarding the use of development finance inflows. Their findings indicate that both FDI and remittance have similar levels of significant positive effects on economic growth, whereas the effect of ODA is not straightforward. The existing body of literature, however, advises us to disaggregate ODA and holds that least developed and middle-income developing countries face different problems and need differentiated strategies, as Benmamoun and Lehnert. (2013) has shown. Therefore, in our study, we intend to disaggregate ODA into grants and loans and determine if least developed and middle-income countries face the same problems and thus require the same foreign capital inflow strategy.

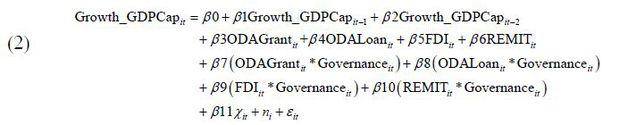

To examine the impact of distinct external capital inflows consisting of two types of ODA (official grants and official loans) and two types of private capital (foreign direct investment and remittances) on the economic growth at two stages of development (middle-income and least developed countries), we use the following estimation models.

Growth_GDPCapit is the dependent variable; Growth_GDPCapit-1 and Growth_GDPCapit-2 represent the lagged dependent variables in the previous periods; ODAGrant, ODALoan, FDI, and REMIT all represent key independent variables; Xit represents the control variables; ni is the unobserved time-invariant country-specific effect; and Ɛit is the error term.

The two equations are basically identical, except that equation (2) has several interaction terms between governance and each of the four different types of development finance flows added to equation (1). This is done to test the hypothesis that each of the four different types of development finance flows is effective only in countries with good governance, as Burnside and Dollar (2000) and Collier and Dollar (2002) asserted. Equation (2) here would be used if the governance variable is effective despite the fact that each of the four different types of development finance inflows is statistically insignificant. In such cases, development finance inflows could be effective through interaction with good governance.

Equations (1) and (2) overcome the shortcomings of the oversimplified Benmamoun and Lehnert (2013) model by including the omitted variables critical for economic growth. These are selected after a close examination of Bassanini and Scarpetta (2001) and are physical capital accumulation, human capital measured by the primary school enrollment rate, population growth, trade openness, and governance.

The dependent variable, GDP per capita growth, which is the annual growth rate of the total output of a country divided by number of people, signals the growth of the economy. The key independent variables of ODA grants, ODA loans, foreign direct investment (FDI), and international remittances, all expressed as a share of GDP, represent their respective impacts on the economic growth of middle-income countries and least developed countries. We subdivide ODA into grants and loans to act as separate variables exhibiting distinct economic impacts. FDI inflows and international remittances constitute private financial inflows into the country, and both are measured as a percentage of GDP.

The control variables (Xit) are derived from economic growth theories with the intention to control the other determinants of the economic growth rate and provide an inclusive model, with minimized omitted variable biases. The Solow-Swan model, a simple neoclassical growth model, postulates that economic growth is the result of capital accumulation and technological progress. Capital accumulation is largely grouped into physical capital and human capital. Physical capital accumulation, one of the main determinants of output per capita, measures the investment rate of a country. In alignment with Bassanini and Scarpetta (2001), we measure the accumulation of physical capital by gross capital formation as a share of gross domestic investment in GDP. Human capital, which represents the labor force, is considered to have significant impact on economic growth as there is a high correlation between a skilled labor force and technological progress. In this empirical study, we use the net primary school enrollment rate as a proxy for human capital.

In the macroeconomic context, other variables pertaining to economic growth include trade, the inflation rate, population growth, and governance, as in other growth studies (Barro, 1996; Bassanini and Scarpetta, 2001). According to the neoclassical growth model, increasing population growth has a negative effect on economic growth, as a higher rate of population growth implies shared capital among a larger number of people. A country’s governance, derived from the Country Policy and Institutional Assessment (CPIA), World Development Indicators, consists of four clusters: Economic Management, Structural Policies, Policies for Social Inclusion and Equity, and Public Sector Management and Institutions. We use the sum of the four CPIA clusters, with a range of 1 to 16 points. Trade, expressed as the sum of exports and imports of goods and services measured as a share of GDP, has often been stressed as having a significant influence on economic growth. The inflation rate, as measured by the consumer price index (CPI), is also controlled for its association with economic growth. Lower or stable inflation rates suggest reduced uncertainty in the economy and thus a well-functioning price mechanism.

The lagged dependent variable, which is GDP per capita growth in the initial year in our model, is considered under the assumption that GDP per capita of the given initial year can have a consequent impact on the GDP per capita of the following consecutive periods. The use of a lagged dependent variable, akin to the four international capital inflow variables (ODA-Grant, ODA-Loan, FDI, and Remittances), however, creates an endogeneity problem which arises from the possible reverse causality between the dependent variable and the key independent variables. To overcome this endogeneity problem, we use the generalized method of moments (GMM) estimation method.

System and difference GMM estimators are powerful tools to estimate dynamic panel data models, using instruments which are available from within the system of equations, without external instruments. System and difference GMM estimators are designed for panel analyses of short time periods (t) and large elements (N). More specifically, they are suitable in situations such as when the dependent variable is likely to be influenced by past variables or when independent variables are not strictly exogenous and may be correlated with past and current realizations of error.

The GMM estimation method is adopted here because this study is confined to a relatively short period, ranging from the year 2000 to 2015, an intended selection to estimate the sheer effect of ODA, which once was highly contingent on diplomatic purposes in the early 1990s. Moreover, our concern about endogeneity calls for the need to adopt GMM estimation as an efficient methodology to conduct the hypothesis test. Several studies of donor policies for aid allocations to recipient countries show that donor countries explicitly consider the income level or growth rate of each recipient (Dollar and Levin, 2006; Lee and Lee, 2014; Bandyopadhyay et al., 2013). Private capital inflows to developing countries are also determined in consideration of the economic growth of the host developing countries. Furthermore, the dependent variable, GDP per capita growth, is largely affected by that in previous years.

The GMM uses first-differences to transform equation (1) into:

where ∆Growth_GDPCapit = Growth_GDPCapit − Growth_GDPCapit-1 and so on for the other variables.

By first-differencing the regressors, the difference GMM eliminates the unobserved country-specific effect because the disturbance ni does not vary with time ( ∆ni = ni − ni = 0 ).

The difference GMM helps to overcome endogeneity using the first-differenced values of the explanatory variables as instruments. The system GMM, on the other hand, estimates concurrently two distinctly instrumented equations: the first-differenced equation (2) (i.e., equation (3)) and level equation (1), the two equations being distinctly instrumented. The use of the system GMM depends on two conditions: (i) the validity of these additional instruments, and (ii) the absence of a second-order autocorrelation.

In our study, where the number of least developed countries with full data is rather limited (23), we use the difference GMM (3), as the system GMM employs too many instruments. We utilized both the difference GMM and the system GMM to test and compare the consistence and efficiency of the model. Considering the Sargan test and AR(2) test, both methodologies proved consistent. However, the difference GMM proved more efficient than the system GMM in our study. By employing fewer instruments, the difference GMM kept the number of instruments below the number of groups (23). Furthermore, in order to ensure that the number of instruments remains equal to or less than the number of groups (23), we also ‘collapsed’ the instruments by combining instruments through additions into smaller sets. This offers the potential advantage of retaining more information, as no lags are actually dropped as instruments.

These models are applied to the panel data of 48 least developed countries (Table A1) and 89 middle-income developing countries (Table A2) and over the period of a decade and a half, from the year 2000 to 2015, for the following three main reasons. First, private capital inflows in least developed countries only began to show a significant increment in the early 2000s. Second, in agreement with Hlavac (2007), this period begins more than a decade after the end of the Cold War and thus is likely to be unaffected by the strategic and political purposes of foreign aid. Third, the period covered coincides with the period during which both ODA donors and recipients actively pursued the Millennium Development Goals in developing countries by mobilizing both ODA and external private capital inflows. Any empirical findings with the data from this period would offer useful lessons regarding the implementation of the Sustainable Development Goals (2016-2030).

To test the severity of multicollinearity among the explanatory variables, we examined the variance inflation factor (VIF), which showed a mean VIF figure of 1.69, confirming that the predictor variables are not linearly related.

The summary statistics are provided in the following tables for the least developed countries and middle-income developing countries, separately:

Although it is more efficient and consistent to estimate the parameters using the GMM estimation method, pooled OLS and fixed effects estimators are also obtained to compare the results with those of the GMM estimators. The estimators for the least developed countries are presented first.

Note: Robust standard errors in parentheses. *** p<0.01, ** p<0.05, *p<0.1.

The estimators of the difference GMM (equation 3) (column 3) and system GMM (equations 1 and 3) (column 4) for LDCs are distinct from those of the other estimation methods (pooled OLS and fixed-effects panel data). The Arellano and Bond test rejects the automatic serial correlation in time series, and both the Sargan and Hansen tests confirm that the overidentification of IV restrictions and the adopted IVs are adequate. The system GMM uses too many instruments, especially compared to the number of groups, and therefore the coefficients must be biased. Hence, we prefer the difference GMM results.

For LDCs, of the four different types of international capital inflows, only ODA grants and remittances showed positively significant effects on economic growth at the 5% and 10% significance levels (column 3), respectively, confirming our first hypothesis only partially.

Result of the H1 Test: For the least developed countries, ODA grants and remittances contribute most to economic growth.

In contrast, ODA loans showed significantly negative effects on growth, and FDI showed statistically insignificant effects on economic growth. These findings imply that for LDCs, remittances and ODA grants constitute the only foreign resources able to exert a significantly positive impact on economic growth during the observed period. This finding differs from that of Benmamoun and Lehnert (2013), where it was found that only remittances are significantly effective development flows for LDCs. Our finding is different from the assertion that aid for Sub-Saharan African countries is wholly ineffective and therefore should be ceased immediately (Moyo, 2009). Our finding also stands in contrast to the conditional ODA effectiveness theory, which states that ODA is effective only when aid recipients have sound economic and political governance (Burnside and Dollar, 2000; Collier and Dollar, 2002; Kosack, 2003). Our finding confirms that ODA grants are effective irrespective of the governance status in least developed countries (LDCs), consistent with findings of Clemens et al. (2004).

We presume that such differences in our empirical findings pertaining to the effectiveness of aid stem from the disaggregated analysis of ODA (between grants and loans) and recipient countries (between LDCs and MDCs). The negative association between ODA loans and economic growth in LDCs compared to the positive relationship between ODA grants and economic growth in LDCs can be explained by the higher costs of loans (obligations to repay the principal and interest) and the weaker government capacities in LDCs to select investment projects with high rates of return and implement them efficiently.

In the difference GMM result (equation 1), the governance variable is a statistically insignificant variable, like other control variables. Therefore, it is meaningless to test the robustness of our estimation based using equation (3), with the interaction term of governance applied to ODA loans, FDI, and remittances (equation 2). The governance variable may not contribute to economic growth in LDCs, as the range of the difference in the variable across countries and in time periods is relatively narrow, while substantial governance improvements in those countries would take many years, i.e., beyond the time allocated for this study.

Therefore, we can conclude that for LDCs, ODA grants and remittances were effective in promoting per capita GDP. However, the existence of sound governance in LDCs was not a necessary precondition for the effectiveness of ODA grants and remittances.

Note: Robust standard errors in parentheses. *** p<0.01, ** p<0.05, *p<0.1.

For middle-income developing countries (MDCs), we also conducted a similar dynamic panel regression analysis using the difference GMM (equation 1) and system GMM inflows (equations 1 and 3). Again, the difference GMM estimators for MDCs (column 3) are distinct from those of other estimation methods (pooled OLS and fixed-effects panel data). The Arellano and Bond test rejects the automatic serial correlation in the time series (except AR (1), as often observed in many studies, and over concerns about GMM, the AR(2) test is more important (Roodman, 2006), while both the Sargan and Hansen tests confirm that the overidentification of IV restrictions and the adopted IVs are adequate.

The results for MDCs (equation 3) are quite different from those for LDCs. Foreign direct investment (FDI), as hypothesized, proved to be the only significant foreign capital inflow showing a positive impact on economic growth at the 1% significance level irrespective of the status of governance in the MDCs. This finding is supported by the system GMM (column 4) outcomes, though it differs from that of Benmamoun and Lehnert (2013), who did not find any type of international development finance flow having a significantly positive impact on economic growth.

In contrast, international remittances had a negative impact on growth but were insignificant even at the 10% significance level. Likewise, both types of ODA variables (grants and loans) are statistically insignificant irrespective of the status of governance. The result can be interpreted as follows: when FDI inflows increase by 1%, the per-capita income growth of MDCs rises by approximately 0.565 percentage points.

This shows that FDI has a substantially positive impact on the economic growth of MDCs.

Our empirical finding of a positive impact of FDI is consistent with several widely cited studies which provided evidence of a positive causal link between FDI and growth in developing countries in general via the transfer of knowledge and the adoption of new technology as well as additional investments (Hansen and Rand, 2006). However, the uniqueness of our finding is that while FDI in LDCs did not have a positive impact on their per-capita income growth, FDI for MDCs showed significant positive impacts on their per-capita income growth irrespective of the status of their governance. We suspect that the difference between MDCs and LDCs may be due to the fact that MDCs in general have sounder and better levels of governance in comparison with LDCs, which has worked better for attracting and taking advantage of FDI. Such distinctions in our findings may originate from the disaggregated analysis of developing countries between LDCs and MDCs, in contrast with the overall research on developing countries in general in the past.

One of many previous studies on the impact of FDI on economic growth of developing countries located in Africa estimated it to be positive in most countries but statistically insignificant (Adewumi, 2007). The statistical insignificance in this earlier study can be explained partly by the inclusion of several least developed countries in the sample and partly given its use of different time periods (time series data from 1970 to 2003), during which the proportion of foreign direct investment inflows as a percentage of GDP was virtually limited and started to increase at a fair rate only in the early 2000s (World Development Indicators, World Bank).

Thus, the positive and significant coefficient of FDI for MDCs implies that there is a positive effect of FDI on the growth of middle-income developing countries, confirming the validity of our second hypothesis:

Result of the H2 Test: For middle-income developing countries, foreign direct investment contributes most to economic growth.

Given that the governance variable by itself is statistically insignificant in promoting economic growth of MDCs, there is no strong motivation to analyze the effect of governance and how it interacts with each of the four different types of international capital inflow variables.

Result of the H3 Test: For LDCs, sound governance is not a prerequisite for ODA grants to become effective in promoting their economic growth. For MDCs, the most effective type of international capital inflow to MDCs is FDI, irrespective of the soundness of governance.

The insignificant role of governance may be due to the many missing observations, especially during the early 2000s, and the rather short period of the analysis to reflect governance changes.

To check the robustness of our test as to whether soundness of governance is a prerequisite of our findings, we applied different measures of governance instead of the total CPIA score. However, these results did not have much significant difference. (These results are not shown here but are available upon request.)

To test the robustness of our test results, we also applied an average value of a much longer period (i.e., 8 years) twice in each country for the four different types of foreign capital inflows to run the difference GMM equation (3). The results show that no capital variables are significant for LDCs; however, only the FDI variable is significant for MDCs, partly supporting the robustness of our basic model using capital inflow observations for every year.

By means of a dynamic panel regression analysis, we studied the effectiveness of different types of ODA and private capital inflows (grants, loans, FDI, and international personal remittances) on economic growth in both middle-income developing countries (MDCs) and least developed countries (LDCs), separately. The literature did not focus strongly on LDCs, which were overshadowed by the rapid economic growth of emerging economies, which drew much scholarly attention. This research is meaningful because it analyzes the subject in a disaggregate manner. First, it compares the impacts of different types of external capital inflows on both MDCs and LDCs separately. In addition, the study disaggregates ODA into ODA grants and ODA loans, as previous studies have shown that they have different degrees of effects on the economic growth of developing countries.

Foreign capital inflows into developing countries, however limited they may be, constitute an important source of investment for their economies. However, not all types of foreign capital inflows into developing countries contribute to their economic growth by the same degree; in fact, some types of development finance inflows can harm the economy in a poor institutional setting, as shown in previous studies. Therefore, this research has policy implications for both MDCs and LDCs regarding the optimal selection of the specific types of development finance inflows that contribute most to their economic growth.

The empirical finding of this study indicates that out of all types of development finance inflows, remittances and ODA grants contribute most to the economic growth of LDCs irrespective of the status of their governance. As shown in the difference GMM estimations, ODA grants and remittances display the most statistically significant and positive impacts on the per capita GDP growth of LDCs. This result is not surprising considering that LDCs have easier access to a steady supply of ODA grants compared to other types of foreign capital inflows due to their low levels of per capita income and economic and financial resources management capacities.

For MDCs, unlike LDCs, FDI has the most statistically significant and positive impact on their economic growth. MDCs are generally equipped with some physical and human capabilities to attract, absorb, and utilize foreign capital inflows. Considering that FDI currently constitutes the largest proportion of foreign capital inflows in middle-income countries, it is not surprising that our empirical analysis confirms our intuitive analysis.

Therefore, policymakers in both MDCs and LDCs should review their current strategies and practices designed to attract different types of development finance inflows, and they should attempt to increase the type of foreign capital inflow most suitable to their development stage and situation. From the perspective of advanced economies, such a division of labor will also contribute to the optimal allocation of international development finance capital. Advance countries are advised to focus on providing FDI for MDCs and on offering ODA grants and remittances for LDCs.

Despite the optimal strategic guidelines for selecting different types of development finance inflows drawn from this empirical analysis, both ODA grant donors and LDC recipients should be wary for the corruptive practices related to grant allocation and application. LDCs should also make efforts to use remittance inflows for sustainable welfare improvements for the poor and for investment purposes. Remittances prove effective under sound financial systems and healthy policy environments (Ratha and Mohapatra, 2007). According to the IMF (2005), a country with good institutions can more effectively use remittances as a means of investment in physical and human capital.

A large amount of remittances can be particularly harmful in developing countries as well as in least developed countries, where the economies are small and remittances are high (Gupta et al., 2007). Gupta et al. (2007) suggests that large inflows of remittances in small economies can create a vulnerability to Dutch disease, an appreciation of the real value of the local currency and losses in export competitiveness, both of which have negative impacts on economic growth.

Likewise, policymakers in MDCs should take concurrent measures to overcome the volatility of FDI inflows (Figure 1) and their negative social and economic effects, including the crowding out of local businesses and the expanding income inequity among their labor forces.

Despite the significant findings here, our research is not without limitations. The methodology of our research may be subject to potentially omitted variable bias, as there are several immeasurable factors that may affect economic growth, such as cultural characteristics. These potentially omitted variables can result in biased or inconsistent estimators, as the significant impacts of ODA or FDI may partially be due to other immeasurable factors that may affect economic growth, causing an upward bias, which even the GMM method cannot fully avoid.

Another limitation lies in our inability to include sufficient elements of private development finance inflows, such as portfolio investments, microfinance, and private loans. Data on private foreign loans, including foreign microfinance targeted developing and least developed countries, were insufficient for a rigorous statistical analysis.

, & (2016). Making aid work for education in developing countries: An analysis of aid effectiveness for primary education coverage and quality. International Journal of Educational Development, 48, 37-52, https://doi.org/10.1016/j.ijedudev.2015.11.008.

. (1996). Politics and the effectiveness of foreign aid. European economic review, 40(2), 289-329, https://doi.org/10.1016/0014-2921(95)00127-1.

, , & (1998). How does foreign direct investment affect economic growth? Journal of international Economics, 45(1), 115-135, https://doi.org/10.1016/S0022-1996(97)00033-0.

, & (2000). Aid, policies, and growth. The American Economic Review, 90(4), 847-868, https://doi.org/10.1257/aer.90.4.847.

, & (2002). Aid allocation and poverty reduction. European economic review, 46(8), 1475-1500, https://doi.org/10.1016/S0014-2921(01)00187-8.

, & . (2007). Grants vs. loans. IMF Staff Papers, 54(1), 139-162, https://doi.org/10.1057/palgrave.imfsp.9450002.

, , & (2004). On the empirics of foreign aid and growth. The Economic Journal, 114(496), F191-F216, https://doi.org/10.1111/j.1468-0297.2004.00219.x.

. (1992). Economic growth in Latin America. Journal of development economics, 39(1), 59-84, https://doi.org/10.1016/0304-3878(92)90057-G.

, , & (2008). Does aid for education educate children? Evidence from panel data. The World Bank Economic Review, 22(2), 291-314, https://doi.org/10.1093/wber/lhn003.

, & (2013). Impact of FDI, ODA and migrant remittances on economic growth in developing countries: A systems approach. The European Journal of Development Research, 25(2), 173-196, https://doi.org/10.1057/ejdr.2013.1.

, , & New Data, New Doubts: A Comment on Burnside and Dollar’s ‘Aid, Policies, and Growth’ (2000). American Economic Review, 94, 774-780, https://doi.org/10.1257/0002828041464560.

. (1978). Relative backwardness, direct foreign investment, and the transfer of technology: a simple dynamic model. The Quarterly Journal of Economics, 92(1), 1-16, https://doi.org/10.2307/1885996.

, , & (2009). Effect of remittances on poverty and financial development in Sub-Saharan Africa. World development, 37(1), 104-115, https://doi.org/10.1016/j.worlddev.2008.05.007.

, & (2009). Remittances, financial development, and growth. Journal of Development Economics, 90(1), 144-152, https://doi.org/10.1016/j.jdeveco.2008.10.005.

, & (2006). On the causal links between FDI and growth in developing countries. The World Economy, 29(1), 21-41, https://doi.org/10.1111/j.1467-9701.2006.00756.x.

, & . (2008). Foreign Aid and Market Liberalizing Reform. Economica, 75(299), 524-548, https://doi.org/10.1111/j.1468-0335.2007.00623.x.

. (2003). Effective aid: How democracy allows development aid to improve the quality of life. World development, 31(1), 1-22, https://doi.org/10.1016/S0305-750X(02)00177-8.

(2003). Does foreign direct investment always enhance economic growth? Kyklos, 56(4), 491-508, https://doi.org/10.1046/j.0023-5962.2003.00235.x.

, & (2009). Does health aid matter? Journal of health economics, 28(4), 855-872, https://doi.org/10.1016/j.jhealeco.2009.05.004.

, & (2007). Does aid affect governance? The American Economic Review, 97(2), 322-327, https://doi.org/10.1257/aer.97.2.322.

, & (2008). Aid and growth: What does the cross-country evidence really show? The Review of economics and Statistics, 90(4), 643-665, https://doi.org/10.1162/rest.90.4.643.

(2004). Does foreign aid promote the expansion of government? American Journal of Political Science, 48(1), 77-92, https://doi.org/10.1111/j.0092-5853.2004.00057.x.

(1988). The multinationals’ economic penetration, growth, industrial output, and domestic savings in developing countries: Another look. The Journal of Development Studies, 25(1), 55-82, https://doi.org/10.1080/00220388808422095.

World Development Indicators. World Development Indicators, https://data.worldbank.org/products/wdi.