The Intergenerational Effects of Tax Policy in an Overlapping Generations Model with Housing Assets†

Abstract

Using an overlapping generations model, this paper examines tax policy effects across generations. The model incorporates housing assets separately from capital assets and includes taxes on labor income, capital income, consumption and housing assets. Tax reforms for each tax rate have different effects on tax burdens across generations and the overall efficiency of the economy, leading to different welfare costs for generations. Specifically, raising housing property taxes results in the smallest welfare loss by future generations, as in the model it does not hurt economic efficiency and the tax burden increases mainly for the elderly, who have accumulated housing assets in preparation for retirement.

Keywords

Tax Policy, Life Cycle, Generation, Housing

JEL Code

E62, H22, R21

I. Introduction

Concerns about fiscal sustainability are rising as government expenditures on welfare continue to increase. Specifically, rapid population aging is expected to increase expenditures on pensions, health insurance, and long-term care insurance for the elderly. On the other hand, population aging can slow economic growth and weaken the tax revenue base. As a result, total expenditures are expected to increase more rapidly than total revenue, and government debt is expected to expand.1

Government debt is increased by deferring the tax burden of the current generation, which may ultimately lead to an increase in the tax burden of future generations. However, if the expansion of government expenditures is mainly due to welfare expenditures for the current generation, there could be an intergenerational imbalance between the benefit and the burden. In particular, as welfare expenditures due to population aging are expected to increase sharply, the intergenerational problem of who will bear the burden could become serious. In fact, several studies point out that intergenerational equity has worsened in Korea. Chun (2012) argues that as aging-related expenditures grow, the burden on the current young and future generations will also increase. Moreover, under the current pension and welfare systems, the current generation has less of a burden than the benefit received, while future generations may experience more burden than benefit to secure fiscal sustainability (Choi, 2013; Lee, 2015a).

In the early stages of the development of a welfare system, some difference in burden and benefit between generations may be inevitable. However, fiscal efforts should not seek to maintain or expand this imbalance and should instead seek to ensure financial sustainability. Recently, a tax increase is being discussed to cover increasing government expenditures. In discussing tax policies, it is also necessary to consider how to alleviate the current imbalance structure of the burden and benefit between generations.

This paper examines tax policy effects across generations using an overlapping generations general equilibrium model. I consider housing-related taxes as well as taxes on consumption and income by including housing assets separately from capital assets. In the case of Korea, households have a large portion of their assets as housing assets and hold substantial housing assets in old age. Thus, tax policies on housing assets may have significant and different effects across generations. Additionally, housing assets have a distinct characteristic in that housing assets, unlike capital assets, directly affect the utility of households by providing housing services rather than being used as production inputs. Accordingly, a change in housing property taxes can affect the choice of economic agents differently compared to changes in capital income taxes.

The overlapping generations model here is an extension of that in Yang (2009) and Fernandez-Villaverde and Krueger (2011), and it as well separates housing and capital assets. These studies note that housing plays a role not only as an asset to accumulate for savings but also as collateral under imperfect capital markets. In addition, unlike other assets, housing assets directly affect the utility of households through the provision of housing services. These studies mainly focus on different consumption and accumulation patterns pertaining to housing assets compared to other consumer goods and assets (Gervais, 2002; Yang, 2009; Fernandez-Villaverde and Krueger, 2011; Díaz and Luengo-Prado, 2010). In this paper, I extend this model by introducing taxes on housing assets, consumption, and labor and capital income types.

I compare the effects of tax policy changes on the overall economy and on welfare. According to my model, the welfare losses are lower when raising housing property taxes and consumption taxes compared to tax increases on capital and labor income. An increase in housing property taxes encourages investments in capital assets instead of housing assets and promotes economic growth, which reduces the welfare loss of future generations. Similarly, increased consumption taxes induce capital accumulation and production instead of consumption. On the other hand, increasing the capital income tax reduces aggregate capital and production, resulting in the largest welfare loss.

I also analyze the intergenerational impacts of tax increases along the transition path. An increase in labor income taxes reduces the welfare of the current working age group and future generations who will work and earn labor income, but it scarcely affects the welfare of older people in retirement. On the other hand, taxes on assets have negative effects on the welfare of older people, who have accumulated assets for retirement. In particular, increasing housing property taxes lowers the welfare of the elderly the most because they hold substantial housing assets to consume housing services and finance non-housing consumption in retirement. However, the welfare losses of young and future generations is less than in other tax reform cases because an increase in housing property taxes does not decrease economic efficiency.

Many studies have examined the effects of tax policy on overall economy efficiency and welfare gains or losses across generations using the overlapping generations model. Auerbach and Kotlikoff (1987) examine the intergenerational effects of tax policies on wages, consumption and capital income. Altig et al. (2001) study the welfare effects of tax policy changes between and within generations. In the case of Korea, Kim (2013) examines the tax policy effects to preserve tax revenues which were reduced due to the corporate tax cut of 2008. Overall, the literature on tax policy focuses on taxes on labor income, consumption and capital income, but I introduce housing related taxes, which have not been addressed in the literature.

The remainder of this paper is organized as follows. Section 2 presents empirical findings with regard to distributions of incomes, assets, and related taxes across ages. Section 3 presents the model. Section 4 calibrates the model and shows quantitative results based on the model. Section 6 presents empirical results on heterogeneous preferences for tax policies across generations using survey data, and Section 7 concludes the paper.

II. Empirical Findings

In this section, I analyze the current tax burden across ages using the 2012 (wave 5) National Survey of Tax and Benefit. The survey data provides information about households’ tax burden, including individual income taxes, property taxes, and comprehensive real estate taxes. Using this information, I compare the distributions of the tax burden with those of household incomes and assets.

The distributions of the tax burden across age are closely related to the distributions of income and assets, which are the tax sources. The figure on the left in Figure 1 shows the distributions of total household income and earned income. Earned income includes salary and business incomes. Total income encompasses earned income as well as rental income, interest and dividend income. Both total income and earned income rise when people are in their 20s and 30s, peak when they are in their 40s and 50s and sharply decrease when they reach their 60s. The gap between total income and earned income increases with age, meaning that income other than labor income accounts for a larger share as people age. The figure on the right shows the individual income tax burden, including working income taxes and comprehensive income taxes. The distribution shows that the average income tax burden is concentrated on working age groups under 60 years of age. Similarly to the income distribution, income taxes increase when people are in their 20s and 30s, peak when they are in their 50s, and then decline. After retirement the income tax burden becomes very low.

FIGURE 1.

DISTRIBUTIONS OF HOUSEHOLDS’ INCOMES AND INCOME TAXES (UNIT: KRW 10,000)

Source: National Survey of Tax and Benefit.

Figure 2 shows the distributions of assets and asset holding taxes. Asset holding taxes includes property taxes and comprehensive real estate taxes. Total assets increase gradually with age, peaking when people are in their late 50s. Past that point, total assets decrease steadily, unlike the income distribution, which decreases steeply after it peaks. Even after the age of 70, the average asset size is substantial and close to 200 million won. Net assets, equal to total assets minus total liability, is distributed similarly to total asset and decreases gradually when people are past their 50s. Housing assets account for a large portion of total assets. Similarly to asset distributions, elderly people have substantial housing assets, and those in their 70s have more housing assets than those in their 30s. Accordingly, the tax burden on asset holdings is the largest when people are in their late 50s and remains considerable when they reach their 70s and 80s. These asset-related distributions are distinctly different from the income-related distributions discussed above.

FIGURE 2.

DISTRIBUTIONS OF HOUSEHOLDS’ ASSETS AND ASSET HOLDING TAXES (UNIT: KRW 10,000)

Source: National Survey of Tax and Benefit.

Figure 3 presents the distribution of consumption expenditure across age. Because consumption tax is not surveyed, the distribution of consumption tax is not compared. However, consumption tax distribution is assumed to be quite similar to the consumption distribution, as much of the consumption tax is value added tax (VAT), which can be roughly calculated by multiplying the consumption expenditure by the VAT ratio. Consumption expenditures increase with age, peaking when people reach their 50s. Then, consumption declines, but the level of consumption remains constant in retirement. I also quantify consumption per adultequivalent, which is adjusted for changes in household size across ages. The distribution of consumption per adult-equivalent shows the consumption pattern while controlling for the household size effect on consumption.2 The pattern of consumption per adult-equivalence is smoother than that of household consumption because household size changes across ages account for much of the change in household consumption, especially for young people, who increase household sizes by marriage and childbirth.

FIGURE 3.

DISTRIBUTIONS OF HOUSEHOLDS’ CONSUMPTION PATTERNS (UNIT: KRW 10,000)

Source: National Survey of Tax and Benefit.

These results show that income sources and asset compositions vary across ages; hence, the main source of the tax burden also differs by age. For the working age group, the tax burden is mainly from labor income taxes, while older people have substantial tax burdens on their accumulated assets.

Individuals experience changes in their incomes and asset holdings. Accordingly the tax burden on income, assets, and consumption also changes over the life cycle. The difference in the age-related tax burden is less problematic with regard to intergenerational equity from the perspective of the life cycle than in the cross-sectional analysis, as the differences in income sources and asset compositions over the life cycle are experienced during one's lifetime. Even if the tax burden imposed on some age group is excessive due to unequal tax burdens across tax sources, all individuals experience a life cycle. Therefore, when the entire life cycle is considered, the problem of equity between generations disappears.

However, if the tax structure is changed at some time, the tax policy effect will differ across generations. Because each generation is at a different point in their life cycles, the dynamic effect on their welfare varies from generation to generation depending on the direction of tax policy changes. Which tax rate is adjusted directly affects the tax burden on each generation depending on their incomes and assets at the time of the tax policy change. Moreover, tax structure changes affect the choice of economic agents and the overall economy, possibly leading to different welfare changes across generations.

III. Model

In this section, I build the overlapping generations model to examine tax policy effects across generations. The model includes various types of taxes, such as labor income taxes, capital income taxes, consumption taxes, and housing-related taxes (i.e., housing property taxes and transaction taxes). To study housing-related taxes separately, this paper considers two types of assets: housing and non-housing assets. Non-housing assets are used as input for production, while housing assets are used for consumption of housing services. The model is extended based on work by Fernandez-Villaverde and Krueger (2011) and Yang (2009). For modeling simplicity, I assume that a housing rental market does not exist.3

A. Preferences

Each period, a new generation enters into the model and begins working. Then, the generation retires at TR and can live up to T . The conditional probability of individuals aged t surviving to become age t +1 is st . Here, sT is defined as 0.

Individuals maximize their expected lifetime utility, which is derived from general consumption on non-housing goods ( ct ), consumption of housing service ( ht+1), and leisure (1 − lt ),

where β is a discount factor, η is a risk aversion parameter, and υ is a labor supply elasticity parameter. γ is a parameter measuring the weight of consumption of non-housing goods over consumption of housing services.

Individuals have one unit of time in each period. Before they reach retirement age, each individual makes a labor supply decision at the beginning of each period. If they choose to work, they spend time working as much as lt and earn labor income. Instead, they have a disutility from working. After they retire, they do not choose to work.

The heterogeneity of the labor productivity of individuals comes from age and idiosyncratic shocks. Total labor productivity at age t is θtet, where θt is the average labor productivity at age t and et is an idiosyncratic shock of labor productivity. et is assumed to follow a Markov process, and its transition probability matrix is π(e'|e).

The consumer problem can be represented as

subject to

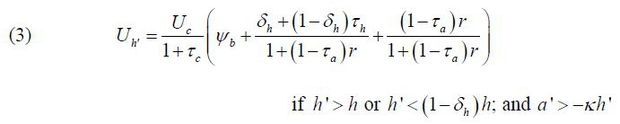

where V is a value function, r is the real interest rate, w is the wage rate for one efficiency unit of labor, and δh is the depreciation rate for housing assets. Individuals receive government transfer b and the new generation who enters into the model receives accidental bequests of ξ. They make decisions about consumption and the allocation of capital and housing assets. Individuals are assumed to derive utility from the consumption of housing services equal to the value of the housing assets held. They can borrow capital but face a borrowing constraint. Borrowing capital is limited to κ of the value of the housing asset held. Here, housing assets are used as collateral. If individuals borrow capital, a' < 0 , I assume that capital income taxes are not paid.

τc, τl, τa and τh denote the consumption tax rate, the labor income tax rate, the capital income tax rate, and the housing property tax rate, respectively. When capital income is positive, a capital income tax is imposed. τ(h, h') is the housing transaction tax that is paid when people buy housing assets and ψb is the the housing transaction tax rate. The transaction tax is paid when the value of the housing asset increases or decreases more than the depreciated value.

Using first-order conditions of the consumer’s maximization problem, I derive the following equations.

Equation (3) shows which costs are linked to housing assets or housing services when the borrowing constraint is not binding ( a' > −κh' ). An increase in housing assets leads to a utility gain from housing services but incurs utility costs from direct costs related housing assets and the implicit opportunity cost of buying housing assets instead of capital assets. When increasing housing assets, individuals pay housing transaction taxes. They will also pay depreciation on housing assets and housing property taxes in the next period. With these explicit costs, they also lose the opportunity to invest in capital assets with a return of (1 − τa)r . If the borrowing constraint is binding ( a' = −κh' ), the value of housing as a collateral is added. As housing assets are increased, they can borrow more capital at a rate of κ using the housing assets as collateral. Instead, the interest cost on more borrowed capital is borne in the next period.

B. Firm

The representative firm produces goods using a Cobb-Douglas production function,

where K is the aggregate capital stock and L is the aggregate labor input. The produced goods are used for consumption by consumers, government consumption, and investments with which to produce capital assets and housing assets. Therefore,

where C is the aggregate consumption of non-housing goods, G is the aggregate government consumption, Ik is the investment in capital assets, and Ih is the investment in housing assets.

C. Government

Governments raise revenue by collecting taxes and run a balanced budget every period. The tax revenues consist of taxes on consumption, labor income, capital asset income, housing property, and housing transactions. The tax revenue is used for government consumption (G) and transfers for households (b).

D. Equilibrium

A competitive equilibrium consists of the value function V (t, a, h, e) policy functions of consumption, capital and housing asset holdings, the labor supply, c (a, h, e), a' (a, h, e), h' (a, h, e), l (a, h, e), aggregate capital and labor inputs, (K, L), input prices, (r, w) and the invariant distributions of consumers, Φ(a, h, e) such that the following hold:

a. Given r and w , policy functions solve the consumer’s problem (2).

b. The firm maximizes its profit and input prices satisfy

c. The goods market clears

d. Capital and labor input markets clear

e. The government runs a balanced budget.

IV. Quantitative Analysis

A. Calibration

The time period for the model is five years. The model has 12 generations, denoted

by t = 1, ···, 12. Each generation enters into the model at the age of 25 (t = 1), and can live up to 85 years old (t = 12 ). The retirement age (TR) is assumed to be 65 (t = 9 ). The conditional survival probability  is from the life table of 2010.

is from the life table of 2010.

The stochastic part of labor productivity is assumed to follow the AR (1) process, i.e.,

,

where  . To estimate this part, I use the labor income of waves 1 to 15 of the Korea Labor

Income Panel Study (KLIPS). To be consistent with the period of the model, labor income

is summed for each five years. The estimates are ρ = 0.81 and σe = 0.35.

. To estimate this part, I use the labor income of waves 1 to 15 of the Korea Labor

Income Panel Study (KLIPS). To be consistent with the period of the model, labor income

is summed for each five years. The estimates are ρ = 0.81 and σe = 0.35.

The age-specific labor productivity is calculated by estimating the age-labor income profile using KLIPS data. The average labor productivity at age t follows the equation

The new generation which enters into the model receives accidental bequests from individuals who die. The bequests are distributed to the new generation following the distribution of net assets of 25-year-old individuals, as estimated from the 2012 Korea Finance and Welfare Survey. The remaining bequests are then given equally to the new generation aged 25.

If individuals decide to work, they work for a fixed number of working hours l , assumed to be one third of their total time. The value of the risk aversion parameter η is set to 1.2, within the range of values used in the literature. α is set to 0.39, the value of the capital income share in 2012. The labor supply elasticity ν is set to 1. Given that the number of working hours is a fixed constant, the value of this parameter does not affect the result. The annual depreciation rate for capital δk is set to 10% and the annual depreciation rate for housing assets δh is 4%. The selected upper limit of the loan-to-value ratio (κ) is 50%.

The annual discount factor β = 0.975 is chosen so that the capital-output ratio in the model matches that of the data. To be consistent with the model economy, output is calculated as GDP minus the value of housing services from the National Account (Fernandez-Villaverde and Krueger, 2011; Yang, 2009). The weight parameter between the amounts of consumption of housing services and non-housing goods, γ = 0.545 , is set such that the share of housing assets among total assets is equal to 63%, which is calculated from the 2012 Korea Finance and Welfare Survey. The parameter of disutility from working, B , is selected to meet the average employment rate from KLIPS, which is 69%.

The consumption tax rate τc is set to 10%, which is the value-added tax rate. The labor income tax rate τl, which includes labor income taxes and social security contributions, is set to 20%, as calculated from the OECD tax database. The housing property tax rate τh is set to 0.106% per annum, which is the actual effective tax rate.4 The housing transaction tax rate for buying housing assets, ψb, is set to 1.3% of the house price, which includes the acquisition tax and related special taxes (Kim, 2015). The model does not explicitly include corporate taxes the firm’ profits, as firms are assumed to be in perfect competition and do not generate excess profits in the model. Corporate taxes are assumed to be imposed on the capital income of individuals that provide capital assets for production. The capital income tax rate τa is set to 36% so that the model can meet the ratio of capital income taxes, including taxes on individuals’ capital incomes and corporate incomes, to output from the data. Government consumption is set to 15% of output.

B. Steady State

Figure 4-6 compares the life-cycle patterns of labor income, consumption, housing assets ( h' ), non-housing assets ( a' ), and the employment rate from the model with those from the data. The data patterns of average labor income, consumption, and employment rate are estimated from the KLIPS data used to estimate the age-labor income profile in the model. The patterns of housing and non-housing assets are estimated from the 2012 Korea Finance and Welfare Survey, as used to calculate asset-related moments for the calibration.

The distributions of housing and non-housing assets in the model are similar to those from the data. The distribution of housing assets is smoother than that of non-housing assets. Young agents initially borrow capital to buy housing assets needed to consume housing services in the model. They then accumulate financial assets while working and later dissave them for consumption in retirement. On the other hand, agents tend to hold housing assets when retired because they still need to consume housing services and can finance non-housing consumption using the housing asset as collateral for borrowing.

The labor income distribution for workers in the model is also close to that from the data. The pattern of labor income is hump-shaped and peaks when people are in their 40s. Working age agents earn substantial labor income, after which labor income decreases after it peaks up to retirement. Because agents are assumed not to work in retirement in the model, retirees do not have any labor income. In the data, however, some older agents continue to work even after retirement age and have positive average labor incomes. Employment rates also have hump-shaped patterns in the data and the model. In the model, the employment rate peaks when people are in their 30s, whereas it is highest when people are in their 40s in the data.

Consumption in the model is flat across ages, similar to consumption per adultequivalent from the data (Yang, 2009; Fernandez-Villaverde and Krueger, 2011). Given that the model does not take into account household sizes, it does not reflect changes in household consumption due to changes in household sizes across ages. Due to this limitation, I do not compare the intergenerational effects of consumption taxes in the analysis that examines tax policy effects across generations taking into account transition paths.

Figure 7 shows the life-cycle patterns of the tax burdens. The labor income tax, capital income tax and consumption tax distributions are similar to the labor income, non-housing asset and consumption distributions, respectively. Labor income taxes are levied on working age agents. On the other hand, the capital income tax burden peaks when people are in their 50s and 60s and have accumulated assets in preparation for retirement. Consumption taxes are constant across ages, similar to the consumption pattern from the model. The distribution of housing property taxes is close to the pattern of housing assets, which increases with age and gradually decreases after retirement. Accordingly, the elderly bear a substantial housing property tax burden. The burden of the housing transaction tax is mainly seen in early and later life. The housing transaction tax burden is highest for young agents because they buy housing assets actively to consume housing services. Thereafter, the transaction tax is gradually lowered and surges again in the last period of life because those at this stage sell the housing assets that they have held. Although the pattern of housing transaction taxes across ages could not be directly compared to that from the data, actual transaction taxes may be levied primarily on young agents, who must buy larger homes for marriage and childbirth. In addition, the transaction tax burden may increase in old age as the elderly downsize their housing.

Table 1 compares the shares of tax revenue from each tax source in the model to those from the data. The capital income tax rate in the model is set to meet the share of capital income tax revenue from the data, but for other tax rates, the shares of tax revenue are not targeted in the calibration. The shares of tax revenue from each tax source in the model are similar to those in the data. Tax revenue on labor income is 12.2% of output in the model, which is slightly greater than that in the data, 10.4%. Housing property tax revenue and housing transaction tax revenue in the data (0.3% and 0.4%, respectively) are similar to those in the model (0.4% of output in both cases). The value-added tax revenue on consumption is 3.5% of output in the model, which is lower than the value of 4.5% in the data.

C. Tax Reforms

In this section, I examine the effects of tax reforms on the economy and the welfare of generations. I consider tax reforms that lead to a 10% increase in total tax revenue by adjusting each tax rate.

Table 2 compares the initial steady states and the new steady states of tax reforms increasing the tax rates on consumption, capital income, and housing property and labor income. I assume that the increased tax revenue is used for government consumption when analyzing the effects of tax policy changes.

With regard to increasing the consumption tax, the aggregate capital (K) and output (Y)6 are increased by 0.04% and 0.17% in such a case compared to the benchmark economy. The increased consumption tax encourages investments in capital instead of consumption, leading to more production. Moreover, when housing property taxes are increased, the positive effects of the tax reform on capital accumulation and production are much greater. Increasing housing property tax rates reduces the demand for housing assets, which may decrease investments in housing assets and output. Instead, the increased tax burden on housing assets could encourage the investments in capital assets and increase production. In my model, increasing the tax burden on housing assets leads to increases in capital accumulation and production by 3.81% and 2.18%, respectively.

On the other hand, if capital income taxes increase, both aggregate capital and production output are lowered. The increase in the tax burden with regard to capital income hinders investments in capital, which leads to reductions in capital accumulation by 7.91% and production by 2.55%. Instead, agents increase their labor supply to compensate for the income reduction, causing the employment rate to increase by 1.11%. If the labor income tax is increased, capital is reduced by 2.03% and production output by 0.99%. Furthermore, the employment rate is lowered slightly.

I compare welfare losses from tax reforms using the concept of equivalent consumption variation (ECV) with regard to how much non-housing consumption (%) should be changed under the benchmark economy in order to gain welfare as much as in the post-reform period. The tax reform of increasing housing property taxes shows the smallest welfare loss, a 2.67% decrease in consumption. Increasing housing property taxes raises investments in capital assets instead of housing assets, thereby increasing production. This positive effect of housing property taxes on the overall efficiency of the economy reduces the welfare loss from the tax increase and leads to the lowest welfare loss among the tax reforms.

Similarly, increasing consumption taxes leads to a relatively small welfare loss, a 3.78% decrease in consumption, because the increases in capital accumulation and production compensate to some extent for the welfare loss due to the tax increase. However, the tax reform choice of increasing capital income taxes results in the largest welfare loss, a 5.52% decrease in consumption. Because the increased capital income taxes reduce capital accumulation and the overall size of the economy, the welfare loss becomes greater.

Overall, in the model economy, the tax reform choices of increasing tax revenues lead to a welfare loss, but tax policy changes that raise housing property taxes and consumption taxes are better than other tax increases in terms of economic efficiency and welfare. The result pertaining to consumption taxes is consistent with those in previous studies. For housing property taxes, newly introduced here, increasing the tax burden on housing assets could allocate resources more efficiently from housing assets not used for production to capital assets, which are production inputs.

Figure 8 shows the welfare changes across generations by each tax reform choice along the transition path from the initial steady state to the new steady state. The X-axis represents age at the time of the tax policy change and the negative numbers denote future generations who enter into the model economy after the tax reform. For future generations, the figure shows the change in lifetime consumption under the benchmark economy in order to gain welfare as much as in the post-reform period, and for the current generation it shows the change in consumption over the period remaining after this time point.

FIGURE 8.

WELFARE CHANGE BY TAX REFORM (UNIT: %)

Note: The X-axis represents the age at the time of the tax policy change. The negative numbers on the X-axis denote future generations entering the model economy after the tax policy change.

Each tax reform has different impacts on different generations. While the increase in labor income tax sharply reduces the welfare of the working age group, the welfare of older people not participating in the labor force while in retirement is hardly affected. Specifically, younger and future generations experience larger welfare losses because they are expected to earn substantial amounts of labor income by working over their lifetimes. Furthermore, the increased labor income taxes reduce output and slow economic growth, which deepens the welfare reduction of future generations.

In contrast, when raising housing property taxes, the reduction in welfare is greater for older age groups. Because the elderly hold considerable housing assets to consume housing services and finance non-housing consumption, the increased housing property tax rate hurts their welfare. On the other hand, increased housing property taxes induce investments in capital assets, which are used for production instead of housing assets, thus expanding the size of the economy. This has a positive effect on the welfare of future generations, and the welfare loss of future generations is accordingly smallest among all tax reform choices.

An increase in capital income taxes decreases the welfare of future generations the most. Contrary to the case of increasing housing property taxes, increasing capital income taxes reduces capital accumulation and production, which lowers the welfare of future generations. For the current generation, an increase in the capital income tax reduces the welfare of those in their 50s and 60s the most because they have accumulated substantial capital assets to finance consumption when in retirement. On the other hand, the effects of increasing the capital income tax on young people, who hold few capital assets, and the elderly, who dissave capital assets for consumption, are relatively minor.

V. Heterogeneous Preference on Tax Policy across Generations

The above results using the overlapping generations model show that the tax policy effects can differ across generations. In this section, I examine actual preferences with reference to tax policy across age groups using survey results from the KDI Generation Study of 2015. Tax policy changes are based on a consensus among members of society at present; hence, it is important to consider the opinions of the current generation concerning policy implementation. The opinions of the current generation on tax policy can be compared to the model results for the current generation.

The survey conducted in order to study intergenerational issues covers 3,500 individuals aged 15 to 79, and each age group, from teenagers to those in their seventies, contains 500 individuals. The survey includes the question “Which tax do you prefer if you need to pay more taxes?” Using the answers to this question, I examine preferred tax policies across age groups.

Figure 9 shows the most preferred tax among consumption taxes, corporate and individual income taxes, and property taxes when respondents are forced to pay more in taxes. In this case, 48% of the respondents choose corporate income taxes. Corporate income taxes seem to be most often preferred, as they are directly applied to the corporate sector rather than to the household sector. Individual income taxes and property taxes were next. Consumption taxes are least favored.

Table 3 presents the factors that affect opinions about preferred taxes. The preference for favored taxes in the case of a tax increase is examined from the first rank to the fourth rank. The preferred tax ranking is the dependent variable and ordered logistic regression is used for the estimation. Main explanatory variables are dummy variables for each age group from their twenties to their seventies. I also include the control variables of household income, household assets and debt, the number of household members, a progressive political view, gender, education, marital status, and dummies for area.

TABLE 3

PREFERRED TAX IN THE CASE OF A TAX INCREASE

Note: This table reports the coefficient estimates from ordered logistic regressions. In columns (2), (4), (6), and (8), gender, education, marital status, regions are controlled. ***, **, and * denote statistical significance at the 1%, 5%, and 10% level, respectively. Robust standard errors are in parentheses.

Regarding corporate income taxes, there were no significant differences in preferences across ages. Every age group selects corporate income taxes as their favored tax if taxes have to be raised. Households with more financial assets do not prefer corporate income taxes, as capital income taxes are levied on capital incomes from financial assets. Households with higher incomes prefer to increase corporate income taxes to other taxes. Moreover, households with a progressive political view are more likely to prefer an increase in corporate income taxes.

For individual income taxes, working age groups do not prefer an increase in this type of tax. Those in their 30s and 40s, whose incomes rise sharply and reach their peak, especially do not favor an increase in individual income taxes. With other control variables, households with greater incomes are less likely to prefer an increase in individual income taxes.

On the other hand, with regard to property taxes, younger age groups prefer to increase this type of tax. In column (6), compared to those in their 70s, other age groups are more likely to prefer to raise property taxes, while younger people, especially those in their 30s, favor an increase in property taxes. Households with more real estate assets do not prefer to raise property taxes because they are expected to bear a higher tax burden.

Consumption taxes are less preferred by the younger age groups. In particular, the preference for increased consumption taxes is lowest for those in their 20s and 30s, whose consumption is expected to increase as their household sizes increase with marriage and childbirth.

Although the model could not reflect all of the factors that influence actual tax policy preferences, the empirical results in several respects are quite consistent with the model results for the current generation along the transition path. The preferences for increased labor income taxes and property taxes are distinctly different across generations depending on their incomes and assets. Increased property taxes are not preferred by the elderly according to the empirical analysis. This outcome is similar to the result from the model, which showed that increased housing property taxes lead to a greater reduction in the welfare of older age groups, who have substantial housing assets. On the other hand, younger age groups do not favor individual income tax increases because people in this age group have significant earned income by working, consistent with the model result, which held that increases in labor income taxes reduce the welfare of working age groups the most. However, unlike the theoretical prediction for capital income taxes, preferential differences for corporate income taxes across age groups are not found in the empirical analysis. All age groups prefer to raise corporate income taxes.

VI. Conclusion

This paper examines tax policy effects across generations. I develop an overlapping generations model that includes taxes on labor income, capital income, consumption, and housing assets. With the model, I compare the effects of tax reforms that increase tax revenues through each tax rate increase. When increasing the housing property tax, capital accumulation and production increase because investments in capital assets are accelerated as opposed to those in housing assets. Similarly, increased consumption taxes also lead to capital accumulation instead of consumption. Accordingly, economy growth is promoted in these two cases and the welfare loss to be borne by future generations is relatively small. Moreover, the tax rate adjusted to increase tax revenues has different effects on the welfare of generations because incomes and assets differ across generations at the time of the tax changes. An increase in labor income taxes reduces the welfare of the working age group but scarcely affects retirees. On the other hand, taxes on assets increase the tax burden on the elderly, who have accumulated assets for consumption. Specifically, raising housing property taxes leads to a greater reduction in the welfare of older age groups, whereas the welfare loss of future generations is the smallest among the tax reform options.

These results show that the tax burden imposed on each generation varies depending on the direction of tax policy changes. Currently, as welfare spending has expanded, there is a growing consensus with regard to the need to increase taxes. The change in tax policy is related to the intergenerational question of who should bear the burden of increasing benefits. Thus, when discussing tax increases, the intergenerational effects of tax policy as addressed here must be considered as a group. However, the model economy in this paper has limitations, and the results should be cautiously interpreted. This paper has assumed that individuals can decide whether to work, but the working hours are fixed at the full-time level. Recent optimal tax policy studies show that the optimal capital income tax is significantly positive with an endogenous labor supply when the income distribution effect is considered (Conesa et al., 2009). This implies that the results here pertaining to capital income taxes may be overestimated. This paper also focuses on the distinctive characteristics of housing assets, which differ from capital assets, but the model here without endogenous housing prices does not take into account changes in housing prices according to tax policies and investments in housing assets for capital gains. In this sense, the tax incidence by housing price changes and tax policy effects on the level of speculative housing demand cannot be explained by this model. Furthermore, this paper does not consider housing market friction from the rigidity of the housing supply in the short run. It would be interesting to incorporate these housing-specific factors more fully into the overlapping generations model and to investigate tax policy effects across generations in future studies.

Notes

This paper revised and developed Chapter5 of Research Monograph 2015-05, Korea Development Institute, 2015 (in Korean).

The debt ratio is expected to increase from 40% of GDP to 62.4~151.8% in 2060 (Ministry of Strategy and Finance, 2015; National Assembly Budget Office, 2016).

Consumption per adult-equivalent is calculated by dividing household consumption by equivalence scales. I use equivalence scales, defined as the square-root of the household size following the recent OECD method.

While Fernandez-Villaverde and Krueger (2011) do not include a housing rental market in their model, Yang (2009) accounts for the housing rental market with a renting shock that makes individuals rent. According to Yang’s results, as the cost of buying a house decreases, households acquire more housing assets instead of renting. This implies that housing-related tax policy effects are greater in a model which assumes a housing rental market than in a model without a rental market.

The housing property tax rate is calculated by multiplying the effective tax rate of local housing property taxes and the comprehensive real estate tax, which is 0.265% (Lee, 2015b), by the ratio of the tax base to the market value, 0.399 (Park, 2014).

As mentioned in the calibration section, output (Y) is calculated as GDP minus the value of housing services. Because this model does not include housing rental markets, I do not explicitly calculate the value of housing services, which can be calculated based on rents actually paid. Instead, I compare tax policy effects on output not including the value of housing services. However, even when the value of housing services is considered, this paper’s main outcomes with regard to the tax policy effects on output would not be affected. If I assume that the rental housing market exists in the model, the rental price on housing services could be derived from the cost of housing services, as determined by equation (3). With rental prices and housing assets, the value of imputed rent could be calculated across tax reform scenarios. According to the calculation results, the changes in the total GDP including output and the imputed rent are −1.15, −2.80, 0.18, and 2.11% when increasing taxes on labor income, capital income, consumption, and housing property, respectively. These tax policy effects on GDP are quite similar to those on output in Table 2, and the results of this paper therefore remain valid.

References

, , & . (2009). Taxing capital? Not a bad idea after all! American Economic Review, 99(1), 25-48, https://doi.org/10.1257/aer.99.1.25.

. (2012). Social Welfare Policy Expansion and Generational Equity: Generational Accounting Approach. KDI Journal of Economic Policy, Korea Development Institute, 34(3), 31-65, in Korean, https://doi.org/10.23895/kdijep.2012.34.3.31.

, & . (2010). The Wealth Distribution with Durable Goods. International Economic Review, 51(1), 143-170, https://doi.org/10.1111/j.1468-2354.2009.00574.x.

, & . (2011). Consumption and Saving over the Life Cycle: How Important are Consumer Durables? Macroeconomic Dynamics, 15(5), 725-770, https://doi.org/10.1017/S1365100510000180.

. (2002). Housing Taxation and Capital Accumulation. Journal of Monetary Economics, 49(7), 1461-1489, https://doi.org/10.1016/S0304-3932(02)00172-1.

. (2009). Consumption over the Life Cycle: How Different is Housing? Review of Economic Dynamics, 12(3), 423-443, https://doi.org/10.1016/j.red.2008.06.002.